Examining the Size of the US Residential Broadband Opportunity for LEO Satcom

February 23rd, 2026

Over the past five years, Low-Earth Orbit (LEO) satellite connectivity has gone from concept to reality. Today, airline passengers stream Netflix over oceans, cruise goers video call from the Arctic circle, and hikers check emails from the top of Half Dome, all while leveraging LEO satcom technology. But even more notably, by subscriber count, is that households all over can access reliable internet connectivity. Industry leader Starlink has grown its U.S. consumer base to nearly 3 million subscribers as of year-end 2025, after initially launching in 2020. That amounts to approximately 2 percent penetration of total U.S. residential connectivity subscriptions after five years of operations.

The extent of LEO satellite technology future scale is hotly debated. Today, LEO broadband faces performance and cost disadvantages versus best-in-class fiber and cable technologies. Consumers come largely from “hardest-to-reach” households where fiber and cable infrastructure does not exist. But in a world where speed and price gaps narrow, where could LEO most realistically win share?

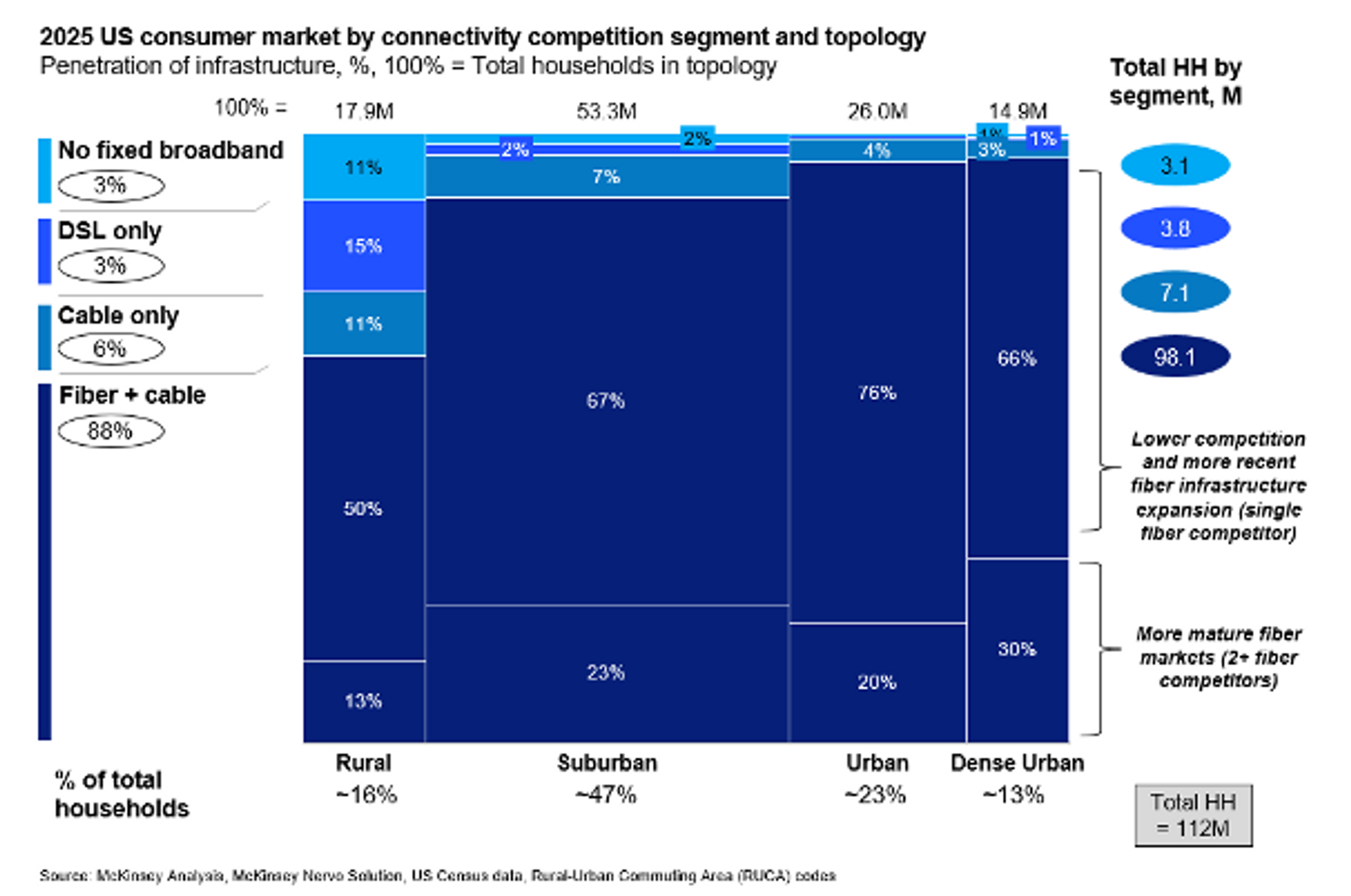

To understand the scale of the LEO residential broadband opportunity in the U.S., we mapped on a census-block level the state of alternative technologies today.

The exhibit illustrates the availability of home internet options across households in the U.S. For example, 11 percent of rural households have no fixed broadband connectivity infrastructure (no copper, no cable, no fiber). Note that this is not the same as adoption: households can have a service “available” but not subscribe due to price, switching friction, or perceived reliability. Note that fixed wireless access (FWA) is not explicitly shown and while may be present, is often significantly lower performing than satellite and wired technologies in rural geographies. FWA is best positioned in urban and densely urban populations where it can more closely compete with wired broadband on performance and cost.

Broadband Deserts

LEO satcom addressability is high for the 6 percent of U.S. households that have no or limited (DSL only) terrestrial broadband alternatives available for home internet subscription. Of this population, termed “broadband deserts,” half have no access to any terrestrial broadband options, and half have access to legacy DSL (copper) technologies. Neither Geostationary Orbit (GEO) satellite offerings (often the only alternative where no terrestrial option exists) nor DSL offerings support the typical performance requirements of modern internet usage such as high-quality video conference and live gaming. FWA may also be available for a subset of this population but falls short of LEO offerings on performance.

LEO constellations offer step-change performance improvements against all alternatives, making the technology well positioned to gain market share. Moreover, these unserved and underserved households are concentrated in rural and fringe suburban zip codes, where LEO connectivity performance is highest. Since the network capacity of the constellation is divided between a smaller subscriber group than in densely populous areas, the subscription base in such areas can scale without concern of traffic volume degrading performance.

Yet, willingness to pay does come into play for households in this population. Over the past decade, income in rural counties remain 20 percent to 30 percent lower than suburban and urban populations according to population research done by the McKinsey Global Institute. Households can face barriers to upfront hardware and subscription prices, though these are expected to drop and are subsidized in some cases. This segment will also continue to shrink, as the Broadband Equity Access and Deployment Program (BEAD) has committed greater than $40 billion to fund terrestrial broadband expansion into unserved and underserved populations, albeit with LEO satcom potentially capturing some BEAD funding.

Competitive Markets

Urban markets: Urban market penetration is limited by constellation capacity and architecture .36 percent of U.S. households fall under urban and densely urban zip codes. Urban and densely urban areas present a difficult consumer market for LEO constellations to penetrate as a primary connectivity choice due to three factors. Urban residents living in multi-unit dwellings lack unobstructed sky views to connect into the constellation, or can face signal obstruction from nearby buildings. High volumes of user traffic hit the limited number of satellites passing overhead at a given time, resulting in slower speeds than demonstrated in regions where capacity is well-matched to user density. And, more than 95 percent of households are fiber enabled, offering customers faster internet speeds often for a lower price than LEO connectivity; FWA offerings are also highly competitive on performance and price. Even if price and performance can be challenged, incumbency – i.e., stickiness – can be strong.

Rural Markets: Rural markets are best topography for LEO to compete with modern alternatives. Around 12 percent of U.S. households are in rural communities that do have access to modern terrestrial broadband alternatives such as cable or fiber. And while there are realistic opportunities for LEO penetration, competition with these two technologies is not created equal:

Where only cable is available, LEO constellations are well positioned to capture the portion of rural consumers who often face cable outages and slow speeds compared to suburban and urban cable users. Notably, LEO speeds often meet (and occasionally exceed) cable in rural segments.

When fiber infrastructure is available, there is a gap in available offerings today; fiber offers a step-change in speed and reliability over LEO and cable and has a lower cost. It is thus unlikely that LEO offerings see more than marginal penetration when fiber is an option, unless it were able to dramatically drop costs.

Yet, LEO connectivity will undoubtedly continue to improve in performance and come down in price. So, what then? Learnings from fiber scaling illustrate that switching barriers exist even when offering a comparable or superior offering. Best-in-class examples of fiber market penetration, where fiber companies offer cheaper and faster services than the cable incumbent, have seen at best ~40 percent penetration over 5 years. LEO providers will face competitive responses from entrenched connectivity providers as those companies take note of meaningful share-taking, offering price cuts and expanded customer “save desks” that give special offers to customers looking to cancel their subscription.

Suburban Markets: The final and largest market segment, suburban households with cable or fiber infrastructure, accounts for 46 percent of total US households. The path to capturing this fiber- and fable-served market is the key question. Today, fiber is superior in performance to satellite across topographies, and cable also largely outperforms LEO speeds in suburban areas, with both technologies often at lower cost to the consumer. A future state of material penetration of LEO technology would require competitive pricing and/or step-change performance improvement.

If LEO providers could come to market with an offer competitive to alternatives on price and performance, they still face switching barriers given the stickiness of incumbent products. As noted above, competitors will react to market share erosion with price cuts and targeted cancellation offers to deter attrition and win back lost ground. To continue momentum, LEO providers need to achieve a materially lower unit cost for terminals (or subsidize, as done in cases today) and cost to add network capacity than has been achieved today. Overcoming the capacity economics in suburban areas is particularly challenging (relative to rural) as the higher density of subscribers requires more capex constellation investment to offer improved performance, or even the same performance, as the subscriber base scales.

Conclusion

Overall, in the U.S. residential broadband market, LEO connectivity offerings are well positioned to win unserved and underserved connectivity markets and, with sufficient price decreases, could realistically penetrate connected rural markets. As the new entrant, LEO players must overcome switching friction observed during connectivity roll-outs, such as the stickiness of cable despite fiber expansion. In the case of a notable gain in market share, LEO providers must also be prepared to react to responses from competitors, including expanded customer save desks, drops in subscription prices, and upgrades of customer speeds in attempts to maintain and regain legacy share.

To scale materially in the U.S. – noting that international markets often have different dynamics – as a primary residential connectivity option beyond rural and underserved markets, LEO providers will need to build a stronger value proposition in suburban markets where highly compelling cable and fiber alternatives exist. This could look like a dramatic price concession, requiring terminal and incremental constellation capacity costs to be greatly reduced, and/or a step-change in performance as next-gen LEO technologies come online.

The shorter lifespan of LEO infrastructure compared to terrestrial broadband is a double-edged sword for achieving these outcomes. On the one hand, more frequent infrastructure replacements add CapEx burden that is not shared by multi-decade terrestrial infrastructure. However, the replacement cycle also creates a powerful iteration opportunity to improve constellation performance with new advances and drive down costs over time. Innovation through iteration has been a cornerstone in the rise of LEO constellations and may well decide its future scale in the consumer market. VS

Brooke Stokes, Partner at McKinsey & Company Fan Gao, Partner at McKinsey & Company Kate Kucharczuk, Consultant at McKinsey & Company

Lead photo: Via Satellite archive illustration