2016: A Key Inflection Point for Ultra-HD

While there have been specific factors at play that have spearheaded the new format in South Korea and Japan, Ultra-HD growth in the region is expected to be replicated at a macro level with the rest of the world. This trend will commence in Western Europe — with its large number of test broadcasts — and North America, before becoming a global phenomenon. April 26th, 2016

Asia stands at the forefront of technological development when it comes to video content, with some of the earliest HD broadcasts occurring in Japan. The same is true for Ultra-HD today, with Sky Perfect JSAT of Japan and KT SkyLife of South Korea having broadcasted commercialized Ultra-HD TV channels for more than a year now. While there have been specific factors at play that have spearheaded the new format in South Korea and Japan, Ultra-HD growth in the region is expected to be replicated at a macro level with the rest of the world. This trend will commence in Western Europe — with its large number of test broadcasts — and North America, before becoming a global phenomenon.

At the end of 2015, 5 Ultra-HD channels were being broadcast in East Asia, consisting of three channels on KT SkyLife’s DTH platform, and two on Sky Perfect JSAT of Japan. Meanwhile in South Asia, those people with the right equipment in the region can reach a few demonstration channels from AsiaSat and Measat, although at this time this is mostly equipment manufacturers and 4K TV retailers.

Today, Ultra-HD channels may appear few; however, the fact that these channels have reached a commercialization phase means we are witnessing a critical inflection point for the format. The transition from testing content and referring to almost theoretical capabilities will now witness real world consumption in consumers’ homes, and it will be Asia that will continue at the forefront of the Ultra-HD transition, specifically in terms of developing Ultra-HD business models. However, as more Ultra-HD channels are broadcast worldwide, “non-Asia” demand will be vastly larger than demand within Asia, at least on a TPEs/channels basis. This is led by dedicated DTH platforms DISH Network and DirecTV in North America. Ultimately, by 2025 NSR expects approximately 785 Ultra-HD channels via satellite, broadcast to DTH, Cable and IPTV platforms, as well as free to air.

South Korea has one of the highest 4K TV penetration rates in the world. It is therefore not surprising that KT SkyLife already has three Ultra-HD channels — UXN, a channel focused on cinema; Sky Ultra-HD1, a general drama and entertainment channel; and Sky Ultra-HD2, a channel dedicated to documentaries. A big pull for subscribers to Ultra-HD is the significant, and growing, amount of local content available in Korean language — a critical component to the success of any channel offering. This is mixed in with foreign — mostly, American — content. KT SkyLife has significant room to grow for Ultra-HD subscriber numbers, and it would not be unrealistic for over half of KT SkyLife’s subscribers to have access to the increasing levels of bouquet channels, with significant transition to higher ARPU packages due to high 4K TV penetration rates and the “network effect” of seeing 4K TVs, which is commonplace around the country.

Elsewhere in Asia, Ultra-HD is moving along at a slower pace, with DTH platforms in India broadcasting limited 4K content — mostly sports. NSR does not expect any channels to be broadcast in Southeast Asia until 2017, and the heavily regulated market in China means a slow pace of development despite high Ultra-HD TV ownership rates.

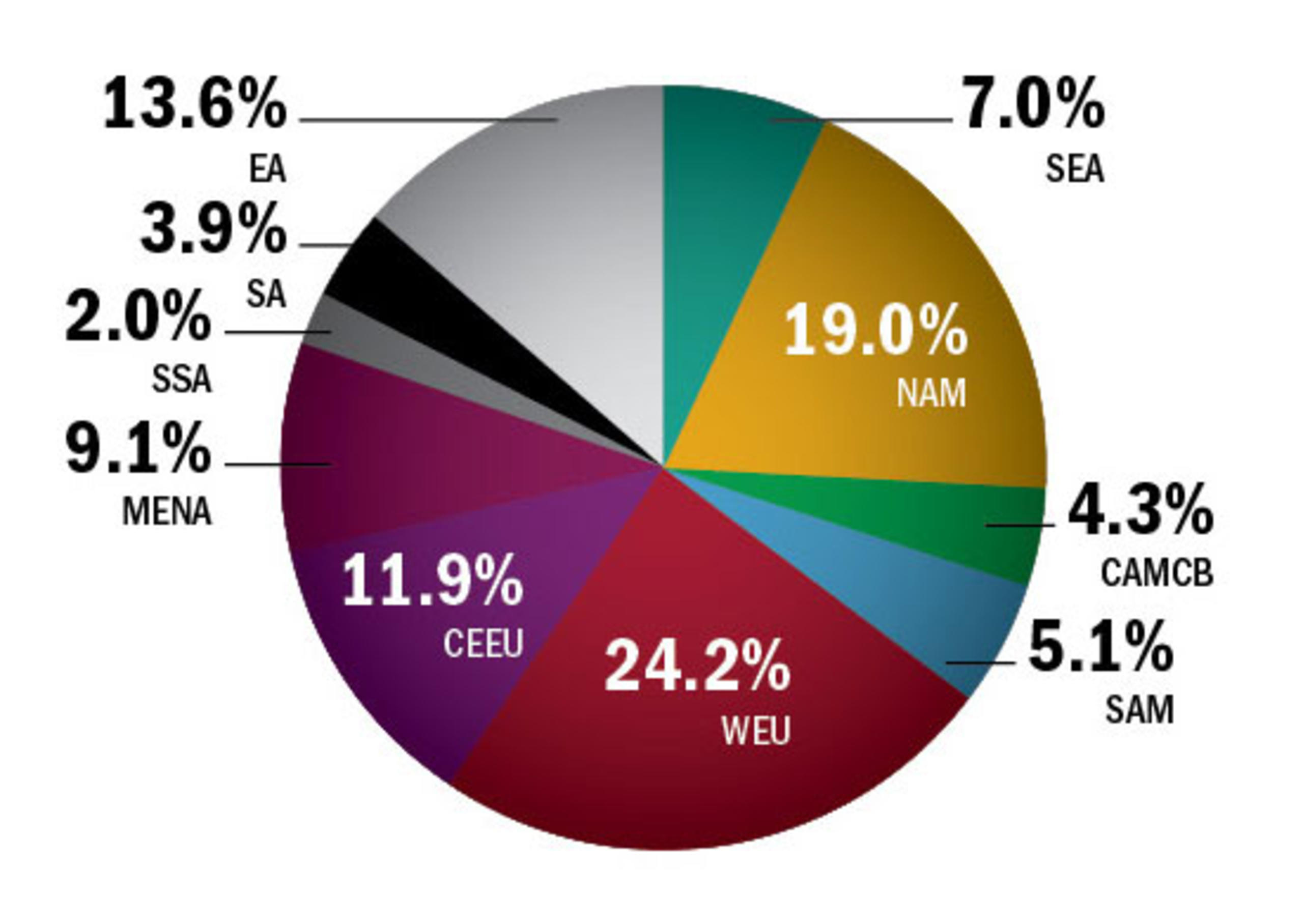

The Future Ultra-HD Revenue Impact

By 2025, NSR expects $280 million in annual transponder lease revenues derived solely from Ultra-HD channel broadcasting. This is a key revenue boost in a market where capacity pricing is stagnant to declining and the impact of OTT is starting to restrain long-term channel growth in some markets.

Currently, pay-TV platforms are offering Ultra-HD channels in their top end packages. This is by and large due to two reasons: offering a free trial so consumers can experience the product, and a retention strategy. Free trials remain a key component of Ultra-HD uptake globally. This is because many consumers are somewhat hesitant to upgrade to Ultra-HD equipment and subscriptions before actually experiencing Ultra-HD in “real life.” Higher resolution and color range simply cannot be viewed on existing screens, and it is difficult to conceptualize before seeing live demonstrations. It is only then when consumers generally see the “wow” factor of the product.

In regions such as South Asia and Southeast Asia, Ultra-HD plays a less important role as revenue growth depends upon keeping and attracting new subscribers. While Ultra-HD certainly plays a role in achieving this, just as important is providing a broad range of SD and HD channels. In many developing regions, SD remains by far the most dominant channel format. NSR’s “Linear TV via Satellite: DTH OTT & IPTV, 8th Edition” notes that in South Asia, SD channels remain at more than 90 percent of the overall market. Nevertheless, opportunities remain to capitalize on high-end consumers who remain less price sensitive to premium content. The traditional strong points of pay TV remain very relevant when it comes to Ultra-HD content.

Bottom Line

The Ultra-HD ecosystem has reached a key milestone in the past year, with commercialized Ultra-HD channels now available driven by pay TV platforms in East Asia. While the market is currently in the early stages of the Ultra-HD consumer rollout, over time, exponentially increasing 4K TV panel penetration and consistently decreasing TV set prices mean that the “chicken and egg” issue for Ultra-HD will become a non-factor within the next few years. While ROI considerations will prove challenging for some time to come, in NSR’s view, it is critical for pay TV platforms to establish long term plans to implement Ultra-HD broadcasts. With an increasingly competitive and crowded video market expected in Asia — and globally — in the future, a failure to innovate in the realm of Ultra-HD will almost certainly result in foregone revenues and a potentially viscous cycle of lower ARPU levels and subscribers being driven to competitors’ innovative new products such as OTT. VS