The global space economy will provide a cumulative space and satellite market revenue opportunity of more than $1 trillion over the next 10 years. There is an expanding need for space-based services to satisfy needs in orbit and on earth fueled by expanding requirements for everything from space-enabled Big Data analytics missions, to commercial crew missions to the ISS, to classic connectivity use cases. While there is a developing space-based, space-consumed economy underway, connectivity-focused use cases will dominate the global space economy revenue picture.

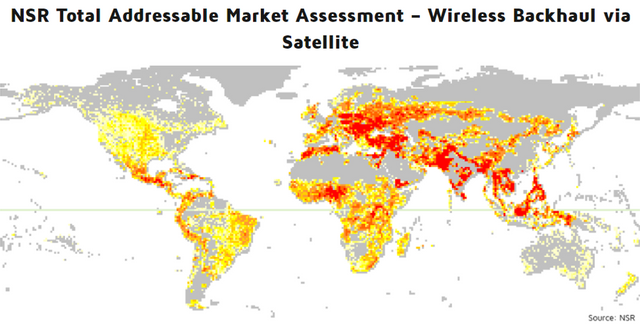

Within the connectivity business, backhaul is THE bet that many programs are hinging their success upon. Indeed, the latest NSR report on wireless backhaul forecasts $25 billion in annual revenue in 2030, propelled by explosive connectivity demand worldwide and post-COVID-19 recovery in the near term. The industry is just scratching the surface of the addressable market with 470 gigabits per second of traffic consumed today, compared with the total potential of 22 terabits per second and expanding due to consumer trends. It is a core target of virtually every current and new satellite capacity provider.

However, NSR is cautious in terms of the much touted revolution that is about to take place. While there have been early tests, commercial satellite backhaul of 5G will still take time to develop. In revenue terms, 4G services will continue to dominate revenue streams over the long term as 5G is concentrated on urban areas. Nevertheless, 35 percent of the traffic by 2030 will be driven by 5G. However, the importance of 5G goes well beyond backhaul of 5G cells as it will facilitate seamless orchestration of satellite and terrestrial networks while opening multiple new use cases.

So while 5G use cases do generate a lot of hype, the key takeaway today is that industry players must not underestimate the transformative power of 5G in how satellite networks are designed. Incorporating and standardizing technologies like Software-Defined Networking (SDN)/ Network Functions Virtualization (NFV) or cloud, 5G network management system will be at the core of how future satellite networks are built, offering the scale and flexibility to optimally operate future Very High Throughput Satellites (VHTS), constellations and software-defined satellites under standardized service orchestration.

Indeed, the overall telecommunications industry is on the verge of a major transformation with the arrival of 5G. Satcom is no different and 5G represents an extraordinary window of opportunity for becoming a mainstream solution. How can satcom maximize this opportunity?

Boosting Adoption and Growth

Previous “Gs” of mobile communications were very narrow, primarily focusing on consumers and operating independently from the rest of communications technologies. But the vision of 5G is much wider, unlocking uncountable enterprise-oriented use cases and offering a framework for integrating all other communications technologies. In this sense, 5G will be transformational in many aspects of the satcom ecosystem: from stimulating demand in many segments, seamlessly integrating satcom in the mainstream telco ecosystem or becoming a tool for optimizing satellite network design and operations.

Today, satellite is a niche solution in the overall telco ecosystem. In cellular backhaul, satcom’s share of total sites is barely 1 percent to 2 percent Satellite’s traditionally higher Total Cost of Ownership (TCO) has obviously been a big barrier for adoption, but even in today’s circumstances, with highly competitive offers thanks to the arrival of HTS and the evolution of ground equipment, many Mobile Network Operators (MNOs) are still reluctant to adopt satcom due to its siloed technologies and processes.

The good news is that things are beginning to change. Satellite capacity price reductions are beginning to unlock growth. Indeed, capacity revenues from data-driven use cases will grow at double-digit rates until the end of the decade. VHTS, Non-Geostationary Orbit (NGSO), virtualization and service orchestration are key technology drivers behind this potential growth. In order to make the most of these trends, the industry must embrace 5G by crafting strategies that are aligned with telco requirements and invest in technologies that seamlessly integrate into the data-driven ecosystem. New price points made ultra-rural network deployments ROI-positive, unleashing solid elasticities and growth.

Finally, from a government response level, UNESCO and the International Telecommunications Union (ITU)’s Broadband Commission for Sustainable Development had set a target of connecting 75 percent of the world’s population to fast internet via cable or wireless by 2025, even before COVID-19 hit. Regulators such as the Federal Communications Commission (FCC) in the United States where more than 6 percent of the population (or 21 million people) have no high-speed connection, are putting forth measures to provide telemedicine, tele-education and other critical services to unserved and underserved communities. Backhaul will be one of the key verticals for satcom growth in the coming years. The COVID-19 crisis might delay some deployments (challenges with financing, installation, or supply chain), but in a world in which communications are more critical than ever, NSR continues to be bullish about the prospects for this vertical despite the current uncertainties.

So what can the satellite industry offer or what is its 5G value proposition apart from providing a pipe? While managed services are an interesting first step in this direction in terms of creating greater flexibility and solving some current challenges like global roaming of mobility platforms, the industry is only scratching the surface of the market’s full potential. By using standardized service orchestration solutions, the industry can enhance its value proposition and become integrated with the telco network with the following offerings and benefits:

• Reduction of configuration and support costs

• Enabling innovative services with shorter time-to-market

• Optimization of OpEx by adopting automation, self-service, and on-demand provisioning of network functions

• Facilitate the integration in hybrid networks

Technology Changes and Strategies

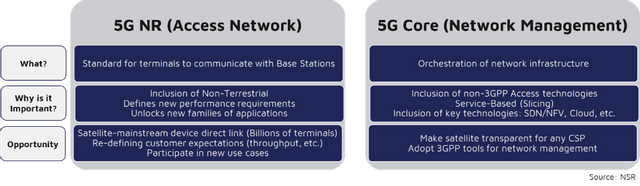

Satcom’s relation with 5G should be bidirectional. It is not only about how satcom can serve 5G use cases, but also how satcom can leverage 5G to optimize network design and operation. Virtualization and cloud are part of the definition of 5G core. As such, operators like SES plan to adopt standardized orchestration, as it offers the capabilities, scale and flexibility to operate their future satellite networks minimizing investment and operating costs.

Satellite requires very specific know-how and uses proprietary standards, making integration with mainstream networks highly complex. 5G has the vision to become a network of networks, integrating multiple access technologies, including satellite. 5G’s standardized service orchestration and the 5G NR extension for Non-Terrestrial Networks will make satellite seamlessly integrable with the mainstream telco ecosystem, dropping barriers for satcom adoption.

5G will also change the perception of what is defined as broadband, boosting bandwidth demand in all segments (even non-5G use cases like consumer broadband). Naturally, backhaul will be among the fastest-growing segments for 5G, leveraging easier integration. Furthermore, regulators are tying strict coverage obligations with new spectrum releases for 5G to avoid a second digital divide.

In a virtualized environment, the relations across the value chain will be transformed with adoption of new business models such as infrastructure-as-a-service that will accelerate. In parallel, multi-orbit domains, expansion in number of beams and users, together with resource flexibility will only make networks more complex. This standardized service orchestration will disrupt how the different steps of the value chain relate to each other, including mainstream communications service providers. With satellite networks now being managed from a 5G core, satellite becomes seamlessly integrable with the mainstream telco ecosystem, eliminating barriers for satellite adoption and unlocking uncountable opportunities. In this scenario, network orchestration will be the new technology differentiator between each network operator. As such, a 5G satellite operator strategy must incorporate this element and be implemented soon in order to cash in on the 5G opportunity quickly.

On the ground equipment side, MNOs have made it clear that enterprise services are one of their key focuses to drive 5G incremental revenues. 5G networking tools are very powerful allowing for network slicing to route traffic optimally depending on the application requirements. If satellite is able to integrate in the 5G ecosystem, there will be numerous opportunities emerging from the unique set of attributes that a satellite overlay can introduce to terrestrial networks (security, redundancy, broadcasting, etc.).

In this context, multiple actors are investing in new developments like Intelsat’s Software-Defined Wide-Area Network (SD-WAN) over satellite access to facilitate the integrability of satellite and terrestrial networks. SES efforts to create a resource control software that interfaces with standard-based Open Network Automation Platform (ONAP) protocols for its O3b mPOWER constellations exemplifies how important 5G will be for the future of network architectures in the satcom world. At the service provider level, accomplishing 5G’s vision of a network of networks will need the creation of new tools like Isotropic’s Datadragon bandwidth management solution integrating hybrid networks, developing concepts like network slicing and optimizing resources at the application level.

Bottom Line

So what does all this mean and what are the prospects for the future in terms of making bets for backhaul and 5G? Quite simply, one in every four USD in Fixed Satellite Service (FSS) satellite capacity revenues for data verticals will be generated from 5G traffic by the end of the decade. According to the GSMA, improved mobile data speed and Improved mobile service coverage are the two primary consumer expectations of 5G. These are obviously in line with what satellite can offer to the 5G ecosystem, contributing to network densification and network extension into remote areas. The potential for growth is extraordinary and NSR forecasts 5G to generate over $21 billion in cumulative FSS capacity revenue by the end of the decade.

5G is much more than just the next “G” with the ambition to be a transversal ecosystem grouping diverse access technologies, including satellite. This is transformational for satcom as it opens the opportunity to become mainstream, with much higher adoption rates.

5G is a unique opportunity for satellite to become a mainstream technology. But to realize this potential, the industry must ensure that it can meet 5G standards both at the network orchestration level and at the radio access level. This would drop historical barriers for satcom such as integration complexities or high TCOs. Network attributes highly valued by both enterprise and customers match very well with what satellite can offer to the ecosystem (enhanced levels of security, coverage, etc.). Network attributes such as slicing or ubiquity ensure a prolific future for satellites in the 5G ecosystem. VS

Lluc Palerm is a principal analyst for NSR. His primary areas of focus are capacity supply, satellite broadband and ground segment, covering key growth areas such as new markets unlocked by HTS, opportunities opened by innovations in ground segment, how satcom integrates in the telecom ecosystem or cellular backhaul and 5G.