As the long-awaited U.S. C-band spectrum auction is finally under way, the revenue growth outlook for the global satellite industry is improving heading into 2021, particularly for the European-listed operators.

With industry revenue growth under pressure since 2015, with the exception of the fixed broadband (mainly in North America) and aviation (pre-COVID-19) satellite segments, Credit Suisse believes an improving revenue outlook could — for the first time in many years — stimulate increased investor interest in the sector.

Credit Suisse’s recently updated Global Satellite database calculated that global satellite revenue growth deteriorated over the past 12 months, down 3 percent Year-Over-Year (YOY) in Third Quarter 2020 (Q3) compared to a half a percent YOY decline in Q3 2019. But more importantly, it improved sequentially, from -5 percent in Q2 2020, helped by easing pandemic headwinds, mainly for Aviation and other mobility, and also due to less drag from video.

Video growth slightly improved sequentially in Q3 2020 to a 7.9 percent decline on constant FX from an 8.4 percent decline in Q2 2020, while improving sequential global satellite mobility, aviation, and fixed broadband revenue growth was enough to offset pressure in the government segment.

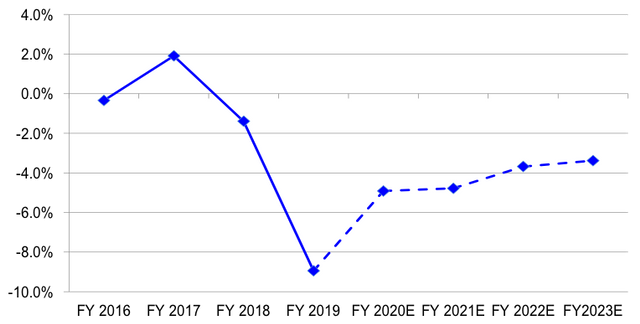

Video Growth Trends to be Less Negative Over 2021-23E

From a European perspective, the outlook for video revenue remains critical to both SES and Eutelsat group growth over the next few years with video still making up over 60 percent of last actual year revenue for both companies. With the reassuring recent Sky Italia renegotiation now behind Eutelsat, an expected rebound in global sports and events in 2021, less drag from U.S. video and incremental emerging market Direct-to-Home (DTH) demand, CS expects video growth trends to become gradually less negative over 2021-23E (Figure 1) — the key to nudging SES 2021 like-for-like revenue growth into positive territory, +1 percent in 2021E, and +2 percent in 2022E.

CS also believe that Ultra-High Definition (UHD) and a lower drag from Standard Defintion (SD) switch off over the next few years could also boost TV transponder demand from 2021E with broadly stable pricing trends globally on a per transponder basis — stable trends in Europe, ongoing pricing pressure in North America, and stability in emerging markets.

Government and Aviation Suffered From Pandemic Effects in Q3 2020

Global satellite government revenue growth slipped into negative territory in Q3 2020, on CS estimates, declining 2 percent, the first YOY decline in many years. SES actually saw a big sequential improvement in government revenue +6.5 percent in Q3 2020 vs. -3.8 percent in Q2 2020, driven by new Medium-Earth Orbit (MEO) and Geostationary (GEO) business signed in the first half of 2020. But it was not enough to offset worsening trends reported by Eutelsat, with lower U.S. government renewal revenues; Viasat, with pandemic effects complicating product manufacturing and shipments; and Iridium, according to CS. Combining GEO with Low-Earth Orbit (LEO) and MEO capacity remains an advantage to GEO-only players.

Unsurprisingly, satellite revenue in aviation including In-Flight Connectivity (IFC), has been hit hard in the past six months due to less global air travel, but Q3 2020 did see a small sequential improvement, still down 17 percent YOY compared to flat in Q3 2019, and down 24 percent in Q2 2020.

Global satellite mobility revenue has actually held up well with SES, in particular, which stated that its Mobility segment performance has been “largely unaffected” by COVID-19 as the vast majority of its contracts are fixed. However, SES expects the impact to be potentially larger going forward.

C-band Auction as a Key Catalyst

CS has published scenarios with total aggregate C-band spectrum proceeds of $47 billion to $61 billion. Both SES ($3.97 billion) and Eutelsat ($0.5 billion) are in line for C-band relocation payments which, according to CS, could be a key catalyst for long-term investors to revisit the European-listed satellites. Although some long-term investors remain skeptical that the C-band process will be completed on time, expected C-band auction proceeds expected by CS to well exceed $10 billion needed to safeguard satellite spectrum payments. As satellite operators are just one year away receiving the first tranche of proceeds, this may be near enough for investors to contemplate the use of the proceeds.

CS Remains Skeptical on the Smallsat LEO Business Models

CS continue to be skeptical on the business case for smallsat LEO constellations, repeating comments it has made many times before. We continue to see key challenges facing so-called smallsat constellations in launching and maintaining a fleet of 700+ satellites in orbit, given the substantial number of launches this would involve over a sustained period of time. The likely cost to completion of these smallsat constellations is several billions dollars, uncertain despite levels of end user demand and returns. In 2019, for example, smallsat company LeoSat suspended its operations due to a lack of investment while OneWeb was also recently recapitalised with the United Kingdom’s government taking a 50 percent stake in the company.

The one LEO operator that is both well-funded and has made solid progress to date, in the view of CS research, is SpaceX’s Starlink constellation. However, as CS recently pointed out — SpaceX’s consumer broadband tracking antenna may need a subsidy of up to $2,000 each to get to a reported $500 retail price point for the customer. As such, CS believes even Starlink faces future challenges in making its broadband business a commercial success.

Satellite CapEx Efficiencies to Continue

In our view, the overall CapEx per amount of satellite capacity is likely to continue to fall. SES sees five-year rolling CapEx falling 28 percent during 2010-22, it currently explicitly guides for CapEx out to 2022. Furthermore, Eutelsat recently said it was replacing three satellites at its key European Hotbird position with two new satellites, EUTELSAT 13F and EUTELSAT 13G, at a lower cost. VS

Paul Sidney is a Credit Suisse research analyst