In recent years, the satcom industry has been going through a transitioning period. It is now more competitive than ever, with this new landscape forcing players to adapt to remain relevant.

Growing High Throughput Satellite (HTS) competition has had a strong impact on the industry, with an increasing amount of telecom traffic moving from widebeam to cheaper HTS capacity. This has contributed to lower regular capacity fill rates and has also had a negative impact on ARPUs and on overall industry capacity revenues. Satellite capacity is increasingly becoming a commodity, resulting in rapidly falling capacity prices.

The pricing environment has shown signs of more modest declines in the past 12 to 18 months, but this has not stopped the average capacity ARPU from decreasing by more than 60 percent between 2014 and 2019. As the erosion of capacity ARPU was only partly offset by increases in capacity leased, the wholesale market value has been in decline since 2014. In 2019, capacity revenues decreased by close to 1 percent, with the decrease expected to be stronger in 2020 due in large part to the COVID-19 health crisis. Despite the recent slowdown in ARPU erosion, this may likely be temporary only as the next major capacity supply influx starting in 2021 is expected to accelerate the downward trend in prices in the middle to long term.

The Impact of COVID-19 on the Satcom Industry

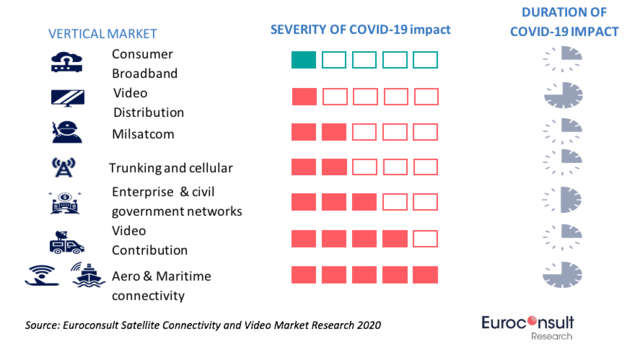

Prior to the current health crisis, our forecasts had anticipated a return to capacity revenue growth in 2020. The impact of COVID-19 has led to a significant revision in our short-term forecast with a return to growth now not expected before 2022. The impact of COVID-19 significantly varies by satcom market vertical with aero In-Flight Connectivity (IFC) and the maritime markets among the most severely impacted in 2020 and with uncertain recovery timelines. Mobility was the fastest-growing segment pre-pandemic. Overall, we anticipate a more gradual ramp up in leased capacity as it takes time to develop a distribution network, roll out services, and open up new market segments. Segments expected to be hit the hardest include aero IFC and cruise.

The other data applications such as consumer broadband and cellular backhaul have been less impacted so far and are expected to see capacity demand ramp up delayed by 12 to 18 months. The cumulative difference in market value over 2020-22 stands at $5.85 billion with mobility verticals (maritime and aero IFC) accounting for around 55 percent of the cumulative revenue difference. The impact also includes a mix of structural market drivers. For example, the downward revision for video distribution is mainly due to heightened price pressure which has led to an acceleration in revenue erosion in mature markets.

At the operator level, companies have been hit hard by the COVID-19 crisis, with some more severely impacted than others. Overall, most publicly traded operators have lower revenues after the first two quarters of 2020 compared to the first half of 2019 with COVID-19 attributed as one of the main reasons for the downward trend. In recent months, a couple of high-profile Chapter 11 bankruptcies have occurred in the satellite industry, and COVID-19 was named as an accelerator. OneWeb, which was planning to launch a constellation of several hundreds of satellites, filed for Chapter 11 protection in March. In July 2020, the U.K. government and Bharti Global committed to pay $1 billion to acquire OneWeb and fund the restart of its operations. In May, Intelsat filed for Chapter 11 bankruptcy to ease a multi-billion-dollar debt and join the FCC’s accelerated clearing of C-band spectrum.

Vertical Integration: A Growing Trend in the Satcom Industry

Prior to COVID-19, satellite operators’ business models had already started to evolve alongside the introduction of HTS systems. Due in part to the multiplication of HTS spot beams and the inherent added complexity of ground infrastructure, in recent years operators have increasingly blended aspects of managed services into their wholesale strategies in order to better manage bandwidth.

The fact that satellite capacity has increasingly become a commodity product, resulting in rapidly falling capacity ARPU globally, has also contributed to changes in strategies, with satellite operators pushed to look for extra revenues. This is even more the case in today’s COVID-19 environment, with satellite capacity revenues negatively impacted in the short term.

Overall, operators are becoming more active in different local markets to enable new service deployment. An increasing number of satellite operators are transitioning from sole wholesale bandwidth suppliers to managed service providers to increase the value added to customers and avoid the commodity price trap. Other operators such as SES and Inmarsat are pushing towards end-to-end network solutions for select markets and/or customers. Moreover, Hughes and Viasat are fully integrated along the value chain.

Vertical integration is a growing trend allowing operators to defend profit margins through differentiation, improve value to end users and grow utilization of large pools of HTS capacity supply. This trend has not slowed down since the start of COVID-19 as highlighted by the recent acquisitions of Bigblu Broadband by Eutelsat in July (the transaction is expected to close by October 2020); and of Gogo by Intelsat in September. This is expected to continue in coming years.

Acquiring Bigblu Broadband gives Eutelsat a distribution arm to distribute and commercialize its broadband-to-consumer product across Europe to complement its wholesale broadband strategy. At the time of the acquisition, Bigblu was the largest distributor of satellite broadband services in Europe. Prior to the acquisition of Bigblu, Eutelsat had already made first steps towards vertical integration notably through the acquisition of video service provider Noorsat in the Middle East and via the launch of its Konnect Africa broadband services.

For Intelsat, the acquisition of Gogo, which is expected to close by the end of March 2021, will make the operator the direct provider of Wi-Fi to more than 3,000 commercial aircraft. Prior to this acquisition, Intelsat had already made some steps toward vertical integration (e.g. investment in AMN backhaul provider and terminal developers such as Kymeta) but they were limited compared to some of the other leading commercial satellite operators such as Eutelsat and SES.

In recent years, SES has increasingly integrated satellite operations, terminals and services apart from selling raw capacity. The operator has notably increased its focus on direct-to-end user services in the maritime (Signature Maritime service targeting ships of all sizes, particularly in the cruise industry), video (notably via the acquisition of RR Media, now MX1) and military markets.

Because of the growing vertical integration observed in the satellite industry, compared to decreasing wholesale capacity revenues, service revenues have grown strongly for operators in recent years as their strategies have evolved. However, despite the increasing focus on managed services, the vast majority, less than 85% percent of the total Fixed Satellite Service (FSS) industry revenues are still derived from wholesale capacity leases. With the introduction of the next-generation of HTS systems, like Very High Throughput Satellites (VHTS), and fully flexible satellites, a deeper transformation of the industry could be expected in the next five years. These new satellites will offer operators flexible capacity which should allow satellite operators to have more control vs. service providers.

Underlying Market Drivers to Enable Long-Term Growth

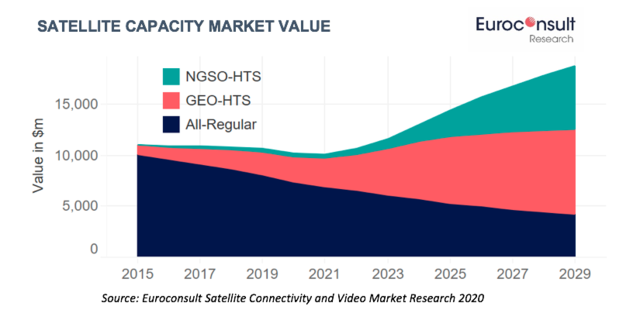

Despite the previously mentioned short term headwinds, underlying market drivers (e.g. growing requirements for broadband connectivity “anywhere, anytime,” and the introduction of higher bandwidth for end users at a reduced cost per bit with new generations of satellites) are expected to enable long term growth projection. From 2022, the satcom market should return to revenue growth and quickly expand in the second half of the decade, with the market value increasing by more than 75 percent by 2029 to just under $19 billion, driven by anticipated demand elasticity in price-sensitive verticals, such as broadband access, rural connectivity, aero IFC and trunking/backhaul.

Several major conditions will be key in supporting the expected growth in revenues in the satcom industry. They include among other conditions the need for significant advances in Non-Geostationary Orbit (NGSO) user terminal technologies, production volumes and capabilities that will be required to help drive higher penetration of addressable markets, the need for satellite operators to deepen their relationships with fixed and mobile network operators as both customers and distributors of satellite solutions, and significant decreases in the cost base of satellite capacity to be translated into lower capacity prices and related services. This will be required to continue narrowing the gap between satellite services and legacy terrestrial networks.

Satellite operators’ needs to adopt new sales models (revenue share, usage base models or co-investment) to stimulate the market take up will also be key. There is a need for operators to take on greater market risk and to support the service ecosystem in order to grow the pie. Satellite operators that have started to look at vertical integration should be better positioned than others to reap the fruits of their investments in a post-pandemic world, where both service and capacity revenues are expected to grow to previously unseen levels. VS

Dimitri Buchs is a senior consultant for Euroconsult.