The space segment has been undergoing a major transformation for a number of years now. Earth Observation (EO) is moving towards a constellation approach, populating new orbit inclinations and altitudes and diversifying sensors. Connectivity focused space systems are now invading Low-Earth Orbit (LEO) along with broadband constellations, and payloads in all orbits are offering more capacity and a higher flexibility.

Right in the middle of the equation to transmit, collect, and distribute data, the ground segment is also making its own revolution. New value creation and CapEx efficiency are at the heart of this journey, which shall see a transformation of the solutions and of the ecosystem at large.

Several drivers are currently reshaping and preparing for the future growth of the $4.8 billion Earth Observation industry. These include: a massive increase in data collection from a larger number and diversity of sensors; a higher data availability, based on a much more frequent data collection of the same locations, and of a reduced time from the data collection to its transmission and distribution (i.e. a lower latency); a ramp-up in the use of automated data treatment, analytics, cloud platforms and storage; and an overall lower cost of data production enabling subscription-based models and the rollout of new value added services.

One noticeable trend when considering the space assets is the transformation of the EO sector to a more constellation-focused approach. Indeed, we expect that over 2,100 EO satellites will be launched as part of about 70 constellations during the next decade, driven by the operators' ambition to provide higher revisit with global coverage. Moreover, a large part of those systems shall be deployed by new organizations that often do not own any legacy ground segment infrastructure.

New EO systems will require both an increase in transmission rates, due to the increasing collection capacity onboard, and more frequent and flexible transmissions in order to minimize the latency between the data acquisition and its availability to service providers and end-users, while optimizing the cost of the ground segment (and global system) infrastructure.

Facing strong potential demand, but also changes in customer requirement, the response of the ground segment ecosystem is responding. At the technology level, it is responding with a combination of innovations being adopted by the industry, and at the commercial level, it is responding with the rise of the Ground Segment-as-a-Service (GSaaS).

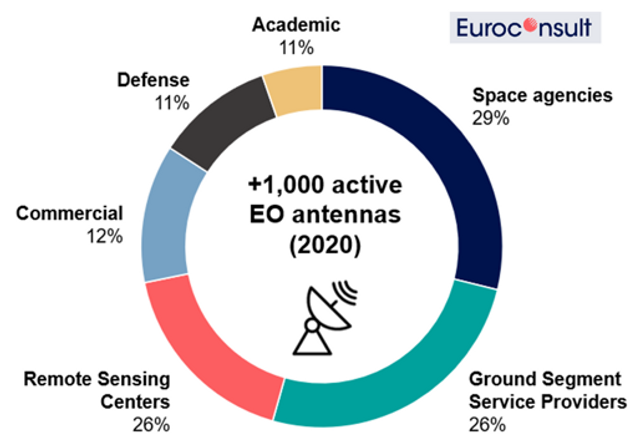

Over the last five years, the shipment of ground stations was mostly driven by the expansion of existing sites with more hosted antennas and the creation of smaller sites (with less than five antennas) in emerging countries. The upcoming government programs and the scaling of GSaaS companies are expected to reinforce these trends. In 2020, Euroconsult estimated more than 1,000 ground stations distributed over about 350 sites worldwide.

GSaaS and Space Agencies to Drive Ground Segment Demand

Limited capitalization and the need for fast time-to-market are the main challenges of commercial satellite operators. As a result, and as the nature of EO systems implies the use of multiple sites with temporary data transmissions, most operators increasingly prefer to focus on the satellite or the payload and outsource totally or partially operations to third parties with an already established network. This outsourcing would limit the direct acquisition of a large ground segment by operators, but would boost the demand from GSaaS companies. One exception shall be the need to comply to certain regulatory obligations, and/or to the needs of certain defense and intelligence clients, which shall push certain operators to keep investing in proprietary facilities.

Ground segment operations require a network flexible enough to support the frequent need for Telemetry, Tracking, and Control (TT&C) and data downlink, and to manage the more frequent changes of the space systems due to the agile (and often low-cost) approach of new satellite operators. If these requirements are not met, the satellite operator will have to deploy its own capabilities to leverage the value of its constellation. That was the case for Planet that installed few years ago 45 ground stations worldwide to operate its hundreds of Dove satellites when the ground service offer was less suited to large small satellite constellation support.

Historical GSaaS suppliers including KSAT and SSC (Swedish Space Corporation) are muting their service from a high-link budget network focused on the pole towards a more diversified network with more antennas at mid-latitude and an extending range of service options. At the same time, new service providers like Atlas Space Operations, Leaf Space, AWS, Viasat, Microsoft, RBC Signals, and Infostellar have emerged and started to deploy global networks, either through proprietary sites or through the mutualization of existing resources. Behind the generic GSaaS appellation, the topology and service offering of each company can significantly differ, and those differentiators should represent key success factors in the coming years. The service pricing is one sensitive factor highly dependent on communication requirements. The arrival of smallsats dropped down the typical price per pass from a few hundred dollars per pass for high link budgets to about twenty dollars per pass for lower-cost communication.

As examples of recent agreements between new satellite systems and GSaaS providers, we could mention the agreement between Iceye and KSAT, the one between Capella Space and AWS and the one between Blacksky and Atlas Space Operations. This being said, these partnerships are not necessarily exclusive, and a satellite operator could work with different providers based on operational and business relevance.

In the new edition of our Ground Segment Market Prospects report, we estimate that the number of active antennas owned by GSaaS companies should almost double by 2025.

The government market should otherwise remain consequent with large investments expected on the ground segment. EO government programs, such as Copernicus and Earth Explorer in Europe or JPSS in the U.S., will motivate Space Agencies to upgrade and expand their existing network.

Some Space Agencies are also planning to complete their existing network with multi-mission antennas suited to smallsat requirements to support demonstrators, academic projects, and smallsat adoption by civil and defense government agencies.

Government customers prefer using proprietary assets due to their sensitivity to governance, security and guarantee of service and try to limit operation outsourcing due to fluctuating demand. The choice of ownership involves investment in network infrastructure to secure data access and protection against cyber-threats. However, they are showing more interest in antenna hosting services to share infrastructure cost.

Growing Interest for Higher Throughput, but X-Band to Remain Most Common Frequency for Data Transmission

Despite the availability of higher frequencies like Ka-band and optical, the X-band should continue to be the most used by EO satellite systems to download their data, while optimization techniques should enable an increase in the actual data rates. The number of satellites to be launched with a Ka-band download capability should remain limited to dozens of satellites in the current decade, most of these being government.

The lack of antennas equipped with a Ka-band chain and the higher sensitivity of the Ka-band to weather conditions continue to limit the adoption of this frequency by satellite operators. However, more operators may opt for it in the future if there is enough availability on-ground. This may lead to a chicken and egg situation with ground operators waiting for demand and satellite operators waiting for supply. Some space agencies and GSaaS providers are therefore taking the lead by adding Ka-band chains and taking advantage of the experience of the upcoming missions to be launched. The S-band is expected to be used by most satellites for TT&C purposes but also to downlink data lighter than imagery like GPS-RO or RF data. Due to the multi-mission approach of ground operators, more antennas should support multiband with at least S- and X-band.

Despite a strong interest in high throughput communication, commercial Optical Ground Stations (OGS) are still far off due to the technology maturity. Indeed, shifting to a higher frequency is a challenge but shifting from RF to optical is another. Indeed, the technology has to be proven and cost-effective both on the ground and onboard the satellite to be commercially available. Moreover, the OGS network must be diversified to increase downlink opportunities to mitigate meteorological disturbances. Collaborative approaches are thus expected between satellite and ground operators for R&D and then for operations.

Flexible Networks to Drive the Average Cost per Station Down

The growth of antennas to be shipped and upgraded results in market growth for the ground segment manufacturing market. The trend toward multi-mission antennas also drives revenue growth for RF equipment manufacturers. However, the average generated value by an antenna is anticipated to decrease over time. On the one hand, ground operators opt for smaller antennas offering more flexibility and lower cost but impacting the link budget. Antennas with dishes between 5 to 10 m are often considered as the best trade-off, decreasing market share for larger and more expensive antennas.

On the other hand, the virtualization of equipment like software-defined radio, network function virtualization, software-defined network enables equipment mutualization, scalability, and more flexibility. Virtualization is already a reality, with a fast adoption by GSaaS providers to support more flexible operations of their ground station network at a lower cost. These software and cloud-based technologies are expected to drive the cost of the RF and baseband chains down, impacting the ARPU of the hardware manufacturers.

This article is the first of a series of two articles in which Euroconsult will review the dynamics and prospects for the ground segment for different vertical segments. VS

Alexandre Corral is the editor of the “Ground Segment Market Prospects” report and a consultant at Euroconsult.