As the COVID-19 situation is improving around the globe, the cruise industry is emerging from a period of near-absolute inactivity. In the early days of the pandemic, contamination clusters onboard cruise ships made the headlines. Shortly after, travel restrictions were adopted throughout the world. This had a very strong negative impact on mobility markets worldwide, especially cruise. As cruises resume, one of the biggest challenges for the industry is to regain customers’ confidence in order to recover profitable fill rates of the vessels.

On the connectivity side, the sanitary measures taken by many countries throughout the world have limited the possibility of installing new satellite communication terminals. The absence of traffic in 2020 also obliged some end users to put their connectivity subscriptions on hold, therefore increasing the number of dormant terminals, or terminals that are installed but not active.

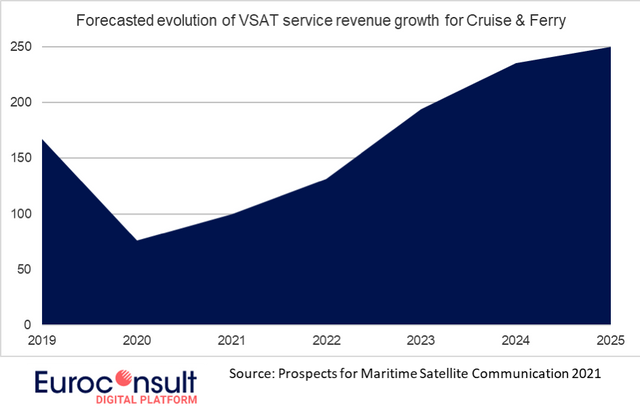

For the cruise segment, it represents a decrease in active Very Small Aperture Terminals (VSAT) by almost 80 percent at the end of 2020 compared to one year earlier. Indeed, when the ships were parked in ports, crew usually relied on terrestrial cellular networks to communicate. As this segment is usually the biggest consumer of bandwidth per vessel, connectivity revenue loss was significant and impacted the bottom lines of service providers that were largely exposed to this market.

As traffic resumes and passengers return to vessels, Euroconsult anticipates a need to boost onboard connectivity due to ever more demanding applications. Passengers expect to enjoy a similar connectivity onboard than onshore. And video streaming is taking a larger share in the applications used, leading to an increasing need of bandwidth. Moreover, as Non-Geostationary Orbit (NGSO) constellations are expected to offer improved connectivity, both in terms of bandwidth and latency, this trend will be supported by the infrastructure. As a result, we forecast a 30 percent CAGR in bandwidth consumption for ships over 25,000 gross tonnage in the next 10 years.

During 2020, the ecosystem of service providers was shuffled with several company restructurings and acquisitions. For instance, Speedcast, the leading service provider on the cruise market went through Chapter 11, although the reasons were in play before the COVID-19 outbreak. Both reorganizations and acquisitions could create opportunities for consolidation of the maritime satellite communications market in the near to mid-term.

The rise of connectivity services based on NGSO constellations will be another factor in the change in the value chain structure. SES plans to launch the first satellites in its enhanced constellation for cruise connectivity, O3b mPOWER, in late 2021.

OneWeb went through Chapter 11 procedure in 2020 and emerged under a new ownership and a one-year delay in their launch planning. However, technology and expected type of service remain mostly unchanged compared to the initial plans. Also, Telesat has confirmed in early 2021 that its 298-satellite constellation built by Thales Alenia Space will be ready for global service in 2024. Additionally, SpaceX announced in March 2021 that the company is officially targeting the mobility markets, including maritime with its Starlink constellation, pending an approval from the FCC.

As NGSO operators hone their planes, such services are expected to challenge the current organization of the market, capturing around 85 percent of the capacity leased for cruise and ferry connectivity by 2030, compared to the 70 percent captured by O3b today on the main cruise lines companies.

The COVID-19 outbreak has greatly shaken the connectivity market for cruise ships with a potentially significant loss of customer confidence. The coming years should see reorganization across the value chain and stabilization for growth of the market, especially as the worldwide sanitary context is improving and as new satellite connectivity technologies will enter the market. VS

Xavier Lansel is a senior consultant at Euroconsult. He is part of Euroconsult’s consulting team in satellite communication markets.