Satellite capacity pricing is increasingly becoming heterogeneous and granular. Demand-supply dynamics, managed services and a looming multi-orbit, multi-band satcom environment are a few of the reasons driving need to assess pricing differently and across space and time dimensions. In its Satellite Capacity Pricing Index report (SCPI7) NSR deep-dives into major aspects modulating bandwidth pricing per application, frequency band and region. Let us look into key pricing trends for the short, medium and long term. While applications and frequency bands exhibit distinct pricing trends per region, we can identify the following general patterns:

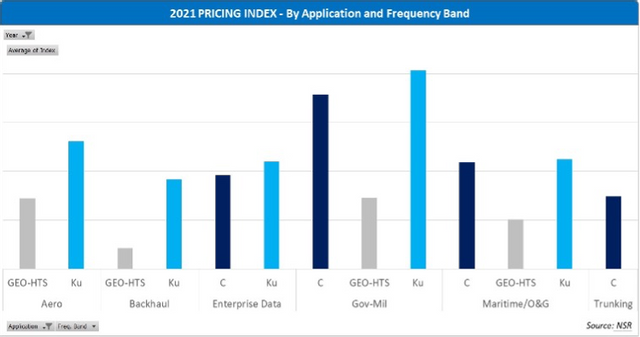

Aero: With distinct adoption speeds, passenger take rates and business models, leading regional airlines are at different stages in the In-Flight Connectivity (IFC) diffusion curve, driving wide disparities in regional pricing. Prior to COVID-19, Ku-band demand was ahead of supply in key battleground regions but prices have now generally stabilized. Aero is a sticky, high-switching-cost business but still poised to become a battleground for both Geostationary (GEO) and Non-GEO players. Current price stabilization may give way to increasing levels of competition and price pressure.

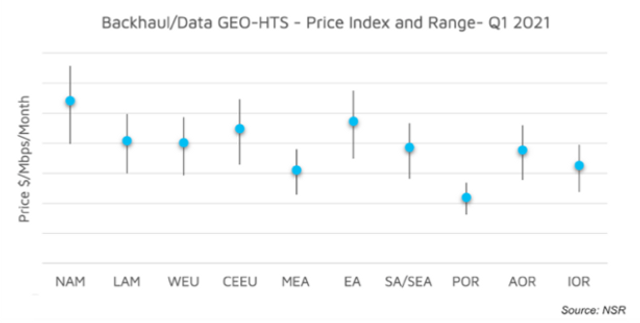

Backhaul: Wireless backhaul is a wholesale volume market commanding high discounts in negotiations. Fixed Satellite Service (FSS) widebeam and High Throughput Satellites (HTS) generally compete in new contracts and renewals exhibiting similar price declines. Mobile Network Operators (MNOs) are increasingly interested in the advantages of HTS to have room for unanticipated grow in traffic without Very Small Aperture Terminal (VSAT) hardware replacement.

Broadband: Consumer HTS broadband is a unique satellite application that requires more granular metrics. In addition to wholesale-level regional pricing, NSR collected retail-pricing data offered across 44 countries by nine major HTS broadband providers to derive metrics that include cost per gigabyte, contention, and effective data rates.

Enterprise VSAT: Continued pressure on FSS pricing remains from HTS. Enterprise VSAT networks leverage the statistical advantages of widebeam coverage, but HTS offerings “pin” customer price expectations, driving the homogenization of widebeam and HTS per-bit pricing in some regions.

Government/Military: NSR sees continuous correction in the market towards the highest range of gov/mil pricing, though this vertical remains the highest priced. Pricing decline slowed in 2021, but pressures will intensify once constellations complete coverage, and VHTS satellites are launched.

Maritime/Oil and Gas: The pandemic seriously impacted the bandwidth-hungry cruise sector resulting in large-volume contract renegotiations and revenue losses for all maritime stakeholders. The energy sector also had a bumpy year, but oil prices returning to reasonable levels point to business recovery. While not expressed by every Low-Earth Orbit (LEO) constellations player, NSR expects that most -if not all- will target energy and maritime segments to increase global fill rates, giving way to renewed price pressure during or after 2022.

Trunking: Declines in C-band trunking price continue on account of C-band repurposing across a few regions and limited alternate uses outside video distribution. Price erosion, combined with high data-rate C-band trunks -which generally use advanced coding and network optimization technologies- continue to push the boundaries of satcom spectral efficiency.

Video Distribution and DTH: The economics of Direct-to-Home (DTH) broadcast are increasingly challenged by consumer’s non-linear viewership. Price erosion continues as broadcasters optimize satellite distribution networks and identify business-case crossing points between satellites and terrestrial alternatives, including HTTP Live Streaming (HLS) cloud-based distribution. C-band repurposing, TV losing advertising revenue and higher compression rates also contribute to erosion.

Medium to Long-Term Impact of LEO Mega-Constellations and VHTS

HTS-LEO constellations will impact satellite capacity pricing differently based on business focus and architectural strengths. SpaceX’s Starlink is about to complete its first shell of satellites, so will soon be competing with established GEO-HTS broadband providers. OneWeb, after emerging from bankruptcy, shifted focus to strategic alliances to reach end users once operational. Telesat Lightspeed will target B2B applications and we shall see how Amazon enters the market with Project Kuiper, which could seek synergies with its cloud AWS ecosystem. SES O3b, which remains the only commercially available Non-GEO HTS system, will expand B2B capabilities via mPOWER satellites and other LEO and Medium-Earth Orbit (MEO) players could enter the picture; so impact on bandwidth supply and pricing will clearly be major and multi-sided.

While the amount of capacity produced by LEO players will be enormous, two aspects need to be considered when analyzing bandwidth supply and pricing trends: Hundreds to thousands of satellites orbiting at low altitude produce high levels of frequency-reuse spotbeam capacity but LEO’s limited visibility of the Earth’s surface reduces addressability for all such capacity supply. This creates highly localized buy/sell opportunities that both operators and educated users will seek to leverage with various degrees of bargaining power. There may be regions like ocean regions where the bulk of LEO capacity goes almost wasted but there could be specific territories where the only way to sell capacity is through a local gatekeeper. So, as measured in NSR’s Non-GEO Constellations Analysis Toolkit, low altitude not only increases spectrum reuse but also reduces addressability.

Naturally, GEOs are also evolving and the simplicity and low costs fixed VSATs will remain key. GEO-VHTS satellites planned by Viasat and Hughes aim to achieve large economies of scale, minimizing the capital cost per production megabits per second. GEOs have more flexibility to steer capacity to high-traffic areas, so as long as production capacity meets projected demand, such programs should be able to push the limits of bandwidth pricing further, this time supported by software-defined capabilities allowing operators to hedge bets on where demand growth will be. This changes the paradigm with the net effect of further reducing the lifecycle cost per bit for satellites that stay in orbit for 15 years or more.

Bottom Line

LEO mega-constellations and VHTS programs will undoubtedly further commoditize satellite bandwidth, a situation that NSR expects will become more evident towards the 2022-2023 timeframe when such programs gain traction and a subset of the LEO constellations complete their first shells and strike commercial distribution agreements.

Given looming disruptions, what happens in the longer term around satellite capacity pricing is less clear but it is possible that we will see a more pronounced departure from region- or even country-level pricing, as ultra-local supply/demand dynamics and pricing power could modulate pricing. Software-defined capabilities are currently focused on addressing network-centric needs (beam steering, orchestration, interference avoidance) but NSR believes that it is only a matter of time before we start seeing “uberization” and Artificial Intelligence (AI) somehow come into the picture of satellite bandwidth pricing as well. VS

Carlos Placido is a senior analyst for NSR.