5G may be the face of the future for mobile in the developed world, but globally, nearly two-thirds of mobile users don’t even have a 4G connection, according to Cisco’s Global Mobile Data Traffic Forecast Update, released earlier this year. Mobile operators “are busy rolling out 4G networks to help them meet the growing end-user demand for more bandwidth, higher security, and faster connectivity on the move,” the networking giant found, predicting a growth rate in 4G connections of 18 percent per year. By 2022, Cisco concluded, when 5G is still in its infancy, more than half (53 percent) of all mobile connections will be 4G — and more than 60 percent in Europe and the Asia Pacific regions. This growth of 4G is already driving a rapidly growing demand for bandwidth. According to Cisco, 4G users typically use three times the data that 3G users do and 10 times as much as 2G users. All that data needs to be backhauled. And that’s where satellite comes in, according to Vinay Patel, senior product line director for cellular backhaul and satellite enabled Wi-Fi at Hughes Network Systems. “The difference [in data demand between 2G, 3G, and 4G] is in the standard: How much bandwidth each of these technologies is able to send to your handset, which directly translates into how much bandwidth you need for backhaul,” he tells Via Satellite.

Higher speeds encourage mobile users to employ more high-bandwidth applications, like streaming video, says the Cisco report, “such that a smartphone on a 4G network is likely to generate significantly more traffic than the same model smartphone on a 3G network.”

And according to Cisco, mobile data demand will grow fastest in developing regions like Africa, with more remote population centers, where terrestrial infrastructure doesn’t reach.

Lower cost satellite connectivity “enables mobile operators to get service to communities that are difficult to reach,” Patel says of Hughes’ backhaul business. These un- or under-served communities don’t just lack a fiber-optic link. “They may not even have roads, they may not have reliable power” and, depending on the terrain, they may not have a line-of-sight connection that’s needed for a microwave backhaul either.

“Most under-served areas face challenges related to geography, infrastructure reliability, and low population density, making it either physically impossible or economically infeasible to use fiber and microwave” for backhaul, adds Karl Horne, SES Networks’ vice president for telco/Mobile Network Operator (MNO) data solutions.

Connecting Iquitos

It was just that trifecta of challenges that beset the remote Peruvian city of Iquitos, the country’s sixth largest urban center, on the edge of the Amazon rainforest, and only accessible by air or water. Local mobile operator Entel was only able to provide Iquitos with “a very basic 3G solution, deployed via a low capacity terrestrial microwave link,” Horne tells Via Satellite.

Then last year, the telecom company partnered with SES and Latin American satellite solution provider Axesat. A year later, Horne boasts, “We are proud to say that ... Entel was offering unlimited 4G data plans throughout the city” and mobile end-users were getting the same 10 Megabits Per Second (Mbps) data download speeds enjoyed buy its customers in the Peruvian capital Lima.

It’s in such remote communities that satellite can really make a difference, explains Hughes’ Patel. “We work with the mobile operators to show them that they can get to these isolated villages or towns … who really want to be connected and deserve to be connected,” he says.

“Wherever there’s a backhaul challenge, satellite can fill that need,” he adds.

Every market is different, which affects the speed and size of new 4G rollouts. “Each operator goes at their own pace,” says Patel. “It all depends on the cost structure in their market and the ability of their users to pay” the higher prices of 4G services.

The antenna used to connect a cell tower with a satellite, the Very Small Aperture Terminal (VSAT), is “a low power operation,” Patel adds. “If you’re energy challenged or if the power supply is unreliable, you can put [a] solar [panel] in there with backup batteries.”

VSAT ground terminals are collocated with the cell tower they serve, and paired with a modem which connects the VSAT antenna to the cellular hardware which actually transmits the signal to handsets all across the tower’s cell. “Mobile operators tend to have multiple generations of equipment at their cell sites,” said Patel. “They might have 2G and 4G (signals coming from the same tower), so the ground station has to support all those generations.”

Hughes’ Jupiter ground system has been “optimized and designed to carry 4G traffic in an efficient manner,” says Patel, adding that it can be used with any available satellite.

The modem translates the incoming satellite signal to a cellular one and vice versa — turning incoming cell signals into radio traffic that the satellite can receive and forward back to the network gateway on the ground.

The ground gateway “takes traffic from thousands of different sites,” explains Patel. “It’s a concentration point where all the traffic is collected and then funneled to the network it needs to get to.”

Increasing capacity is the result of new technologies like High Throughput Satellites (HTS) — and the growing number of Geostationary Orbit (GEO), Medium-Earth Orbit (MEO), and soon Low-Earth Orbit (LEO) constellations. “There are more and more satellites and higher and higher throughput,” said Patel, “The bottom line: There’s a glut of capacity,” which is driving prices down.

“The VSAT is pretty low cost [in capital expenditure terms] and the capacity price is dropping … and that really makes the business case work” for mobile operators, he concluded.

New Cost Structures, New Markets

Lower prices mean satellite can compete more successfully with terrestrial alternatives, which in turn drives up demand, according to Lluc Palerm-Serra, a senior analyst with Northern Sky Research.

“In the past, [mobile operators] looked at satellite as the connectivity of last resort, but with falling prices and technical improvements, it’s become much more competitive,” he says.

It’s not just falling prices that are driving that increased competitiveness: There have also been major technological improvements. “Making even 2G or 3G, let alone 4G, work over satellite can be challenging. There are technical hurdles that must be overcome.”

Throughput capacity has soared. “Five years ago, a ground terminal that could offer 100 Mbps would have been state of the art, bleeding edge technology. Now it is much more commonplace,” Palerm-Serra says.

There’s also been much technical progress in dealing with challenges like jitter, latency, and packet deformation.

These changes come at a time when mobile operators, especially in emerging markets, are expanding 4G services into previously under- or unserved communities, mainly in rural or semi-rural areas, where terrestrial infrastructure may be impractical or highly expensive.

Together they mean that the satellite industry has reached an important tipping point, Palerm-Serra says. “In the past, you might have seen [mobile operators] use satellite [for connectivity to rural/semi-rural communities] because they had a regulatory obligation or a government subsidy to provide that connectivity ... We’ve now reached the point where [mobile operators] can make money off satellite connectivity. They don’t need an incentive or a regulatory requirement any more … That’s driving a lot of additional demand.”

Bending the Cost Curve

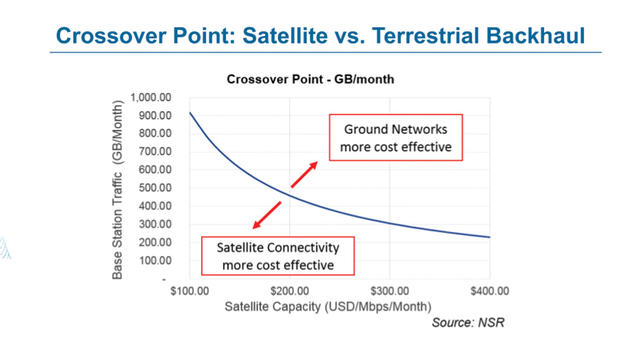

“Currently, bandwidth is priced in in the $2-300 per Mbps per month range, well under a third of what it was just two to three years ago,” he adds.

The $200 figure is a key number, because it’s the point at which a base station with a throughput as high as 500 Gigabytes (Gb) a month becomes — on average — cheaper to run using satellite backhaul than terrestrial, according to NSR figures.

Nonetheless, satellites currently provide backhaul for only 1 or 2 percent of cell sites worldwide, representing annual revenue of about $1.3 billion — approximately 10 percent of satellite industry income this year, a proportion set to grow to 15 or 20 percent in the next decade.

In short, satellite backhaul is “small for the telecom industry, but more significant for the satellite industry” and growing in importance, Palerm-Serra says.

And falling costs can be a double-edged sword for an industry, especially one like satellite, where capital costs are quite literally sky-high. The risk for satellite operators is that their product — bandwidth — becomes commoditized, forcing prices lower.

“With the fall in capacity prices, satellite operators have to work to capture more of the value chain. That means offering more to the mobile operators. It means getting closer to the end user,” says Palerm-Serra.

“Most [mobile operators] don’t know how to manage satellite services … The companies that are going to succeed [in the new, lower cost marketplace] are the ones that make it easy for them by offering end-to-end services” in some cases even including building and maintaining the cell towers themselves, he concludes.

This is what SES calls its “end-to-end managed mobile network solution.” And they tout their standards-driven, transparent approach. “We decided to pioneer an open, standards-based framework for network operations, which helps customers more easily and cost efficiently extend their networks over satellite access links and deliver applications to the edge,” says Horne.

Patel said Hughes was also looking to carry as much of the load as the mobile operators wanted them to. “In those areas like the Americas … where we have [satellite bandwidth] capacity we will bundle the capacity in along with the ground equipment. Where we don’t have capacity, we will find a partner to bundle it if the mobile operator is looking for a one-stop shop, or they can buy it separately, if they want.”

Intelsat is also getting into the new business model, partnering with and investing in Africa Mobile Networks to provide a soup-to-nuts offering for mobile operators it calls a “network-as-a-service” solution. The partnership will fund, build, and operate a series of satellite connected cell tower networks in Africa’s “ultra-rural” areas and then lease access to mobile operators, who can thereby hugely expand their potential customer base without any capital commitment or operational risk.

But being a service-orientated business “is a completely different business model” from the one satellite operators are used to, cautions Palerm-Serra. For instance, they are accustomed to operating with very high EBITA margins, “becoming a service-oriented business will change all that.”

Beyond Backhaul

Beyond the conventional backhaul business, and distinct from the new network-as-a-service offering, the latest frontier for satellite in 4G is an emerging generation of direct to satellite technology — devices that use lightly modified off-the shelf mobile chips and more powerful antenna to get a 4G signal direct from orbit, rather than through a cell tower.

Satellite direct to 4G is still at the experimental stage, says Lluca Palerm-Serra, a senior analyst at Northern Sky Research.

Several companies have such plays, including Lockheed Martin. “We’re now in the process of ground testing, we should be able to start live testing when the satellite is up next year,” Joe Baldasano, systems principal and engineer at the beltway giant tells Via Satellite.

Lockheed is developing both ends of the technology: The ground system, but also the satellite, adds Dawna Morningstar, the company’s director of international and common ground solutions.

The new technology will have two kinds of terminals: A portable one about the size of a small tablet and a slightly larger model, designed for ship- or truck-board use. Both are designed to draw a 4G signal directly down from a satellite, and then provide the short range, high bandwidth connections 4G users are accustomed to via a Wi-Fi connection to a smartphone or other mobile device. The non-portable version will boast “a little larger antenna and a little more power on the transmit side,” says Baldasano, meaning better connectivity and/or more users.

In general, the performance for the end users’ devices is comparable to a conventional 4G phone, he said, “It’s like a big cell tower in the sky.”

The terminal can be controlled either through a physical handset or an application on a smart phone — which shows who’s connected and how much data they’re using.

The technology is designed for multiple use cases, with this in common: “It’s for when you’re outside of range of any cell phone coverage,” says Baldasano.

He says fishing fleets and other maritime assets would be a target market, as would first responders moving into disaster areas where the conventional networks were down or overwhelmed.

There are customers lined up and the first ones will be buying a satellite as well, adds Morningstar.

Lockheed and others are vying to set the standards for this new generation of mobile devices. The ground terminals the company is developing are “optimized for use with a new satellite Lockheed is building,” says Baldasano, “but they can be used with any satellite that can form a beam which meets the GMR-2 4G standards. If it has the right sensitivity and power … and Radio Frequency (RF) requirements then you can receive the signal.”

Lockheed seems to be aiming for the market outcome that others are seeking to avoid: Commoditization.

“There’s no unique hardware in the handset or other equipment on the ground, it’s all off the shelf,” Baldasano says. “The chipset is the one that’s in 4G handsets today. Some of the firmware has been updated to deal with the additional latency you get from satellite … But the whole point is to leverage the 4G ecosystem ... If you use a VSAT, it’s proprietary. Any improvement to that technology, you have to do that yourself. It’s not going to improve unless you make it better at your own expense. With LTE you get to leverage the efforts of the whole ecosystem of developers to improve the technology … In the long run, you get vendor independence and the cost of the equipment will be less because of that ability to reuse [commodity] hardware.” VS