Space in China has historically been associated with the state, and for good reason. The China Aerospace Science and Technology Corporation (CASC) has been synonymous with space in China. With CASC being owned by the Chinese government, this has meant that effectively the entirety of the Chinese space industry, up until 2014, was CASC.

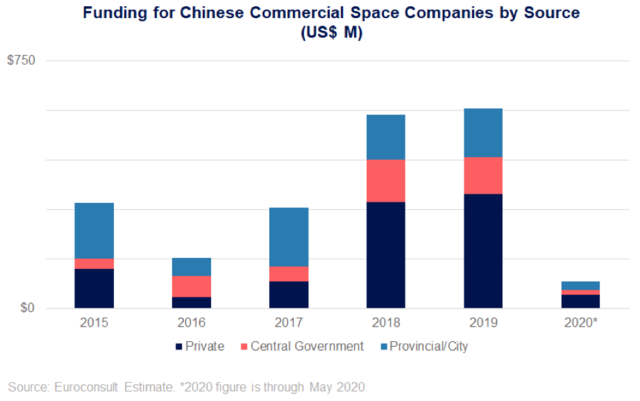

This changed in 2014 as the Chinese government published Document 60, a document allowing for increased freedom of private investment into technologies such as launch and satellite manufacturing. The past six years have seen more than 100 commercial space companies established in China, with these companies having raised more than $1.4 billion (10 billion yuan) in the process, according to Euroconsult’s just-released China Space Industry 2020 research report.

That being said, good things take time, and space is hard. Despite the huge increase in number of startups, most of these companies have yet to move beyond the R&D phase — it takes a few years to develop a rocket. As we move into the 2020s, we are reaching a turning point in Chinese commercial space — the point at which commercial companies commence business operations at scale. Despite the COVID-19 pandemic that shut down most of China for the early part of the year, the country’s space sector has proven surprisingly resilient, with launches having continued at an impressive clip (19 launch attempts by China in 2020, three failures).

What Makes 2020 a Turning Point?

Several factors make 2020 a turning point for the Chinese commercial space industry. While a major reason is the increasing maturity of Chinese space companies, perhaps the single largest reason is geopolitics. As various major commercial space programs in the West have made progress — most notably SpaceX’s Starlink but also Kuiper, and the plethora of smaller companies doing innovative things in smaller verticals — China has seen greater strategic impetus to respond in kind. This was very likely exacerbated by the May 2020 announcement of Starlink signing an agreement with the U.S. Army to test Starlink connectivity.

As a rising global and space power, China has much to lose by letting the United States move far ahead in the NewSpace race. For the Chinese government, the potential loss of allowing the West to move far ahead is far greater than the loss of giving up some control of the domestic space sector via reform and opening up. From the perspective of the Chinese government, even if CASC is capable of keeping pace with SpaceX/Starlink, which is not certain, there is less harm in letting private companies try to help than there is in maintaining the status quo and letting Starlink go global before China has a constellation of its own in orbit. The West’s space progress in 2020 makes this year a key turning point for China.

Other factors are less strategic, but no less important. The fact that many Chinese commercial space companies were established three to five years ago means that now, many of them are reaching maturity and are ready for commercial operations. This is evident in the large bump in funding in 2018 and 2019 (above chart), funding which would have been spent on R&D efforts that are now starting to bear fruit. The increasing interest by major tech companies, a wider variety of universities, and some high schools in the space industry has led to pockets of demand, with several commercial satellite manufacturers counting on academia as a major early source of revenues. The evolution of this larger ecosystem will be essential for a healthy Chinese space industry to develop, as diversity of demand will allow for commercial space companies to be less reliant on subcontracted work from CASC.

The Rise of China’s Commercial Industry

With an increasing amount of government support combined with an increase in funding, the Chinese commercial space sector is on the brink of lifting off. 2020 has seen, among other things, the launch of satellites proving new technologies, an attempt (albeit a failed one) at launching the first Chinese commercial rocket with a payload of greater than 1,000 kilograms, and government rulings in support of development of space applications. In short, despite a shutdown from COVID-19 for much of February and March, China has rebounded strongly in the space sector.

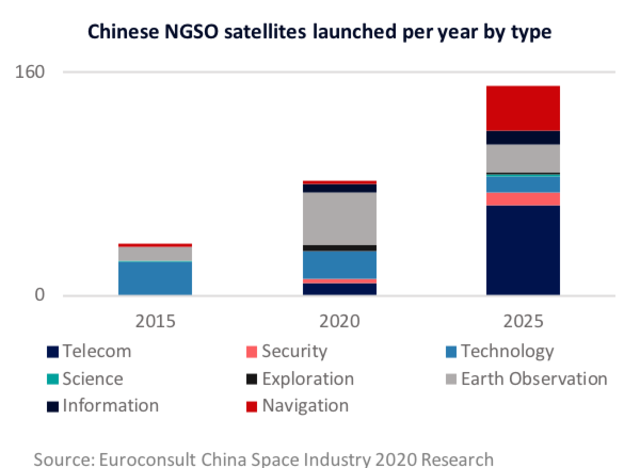

On the satellite manufacturing side, 2020 has seen the launch of the first satellite in the Galaxy Space constellation, a planned constellation of several hundred satellites aiming to address 5G and internet of Things (IoT) demand. Launched to Low-Earth Orbit (LEO) in January 2020, the satellite’s Q-band/V-band payload has a total throughput of roughly 10 Gigabits per second. In an interview around the time of the launch, Galaxy Space CEO Xu Ming noted that he expected non-Chinese constellations to occupy most Ku-band and Ka-band spectrum, and as such, that Galaxy Space hoped to claim Q-band/V-band spectrum for Chinese constellations. Separate to Galaxy Space, Guodian Gaoke has seen several satellites in its Tianqi IoT constellation launched over the past year, while Earth Observation (EO) constellation company Charming Globe has launched multiple EO satellites. Euroconsult expects the number of NGSO satellites launched by China to increase from about 50 in 2015 to more than 160 by 2025.

Separately, satellite manufacturer Commsat announced in May 2020 a $39 million (270 million yuan) round of funding, with the money expected to go towards building a satellite manufacturing facility for an unnamed customer. That the customer is large enough to allow Commsat to justify building a satellite manufacturing facility is a likely indication that the customer is a government project. This represents a significant shift that a commercial company has been selected to provide such products to the government. Satellite manufacturer and aspiring constellation operator LaserFleet also made apparent progress during the year, having provided components for two Xingyun satellites launched in May 2020.

On the launch vehicle side of the industry, 2020 has seen ups and downs, but consistent progress. China’s most advanced (nominally) commercial launch company, Expace, has been the most visible company in the sector thus far in 2020. In April, Expace sold a rocket in a live online auction, fetching more than $5 million for the launch. Maybe more importantly, it attracted several hundred million views in what was perhaps the most successful publicity stunt the Chinese space industry has ever seen. The company has also seen several successful launches of its Kuaizhou-1A rocket, including for multiple commercial clients. Capable of lifting 250 to 300 kilogram to LEO and Sun-Synchronous Orbit (SSO), the KZ-1A has proven itself as a reliable small launch vehicle, with nine successes in nine attempts. Expace also attempted the first launch of its Kuaizhou-11 — a much larger rocket capable of carrying 1 metric ton to SSO and 1.5 metric ton to LEO — though the July 2020 launch attempt failed.

Other than Expace, several Chinese launch companies have seen progress over the course of 2020. Landspace, the second most-well-funded commercial launch company after Expace, has continued to make progress on its Zhuque-2 (ZQ-2) rocket, expected to launch for the first time in 2021. Having completed a $71 million (500 million yuan) round of funding in December 2019, Landspace has focused on developing the TQ-11 engine for its ZQ-2 rocket, with the company having recently completed a 3,000 second hot test on the engine, which represented the longest single engine test of any cryogenic liquid rocket engine in China. Meanwhile, fellow liquid-powered rocket company Deep Blue Aerospace announced a $14 million (100 million yuan) round of funding in June 2020, with this representing roughly the eighth commercial launch company in China to raise more than 100 million yuan. The advancements in the launch sector are expected to continue moving forward, with the Chinese government having passed legislation in mid-2019 that provided some additional clarity for commercial launch companies.

Downstream applications have seen the most major turning point in 2020, however, as China has had several significant developments in this area in recent months. Most significantly, the National Development and Reform Commission (NDRC, 国家发展改革委员会) announced in April the addition of satellite internet to its list of new infrastructures (新基建). The addition of satellite internet to this list sent a powerful signal to the industry that the Chinese government supports the development of satellite internet applications, and has been met with several major announcements in the weeks following. Among others, China Unicom Airnet, a satcom subsidiary of China Unicom, announced 3 new satellite internet products, as well as a location-based service product, with the announcement mentioning the NDRC decision. Commsat also mentioned the NDRC decision in the press release for its aforementioned round of funding, with the company stating that its satellite factory would aim to build broadband internet satellites in line with the ruling.

Other application areas have received a similar boost in recent months, though in some instances this has occurred in late 2019. For example, in November 2019, the China National Space Administration (CNSA) announced that they would start sharing global 16 meter-resolution EO data from the Gaofen-1 and Gaofen-6 satellites for free in partnership with Huawei. Having deployed a global EO constellation over the past decade or so, China is now in a position to push more of its EO data towards the rest of the world. In satellite navigation, in 2020 China completed the third generation of its BeiDou constellation, and has concurrently offered significant support for downstream application development for satnav/location-based services, with this including the development of BeiDou R&D centers in China and elsewhere. Moving forward, we expect China to aggressively position BeiDou as an alternative to GPS, relying partly on geopolitics and financing, and partly on technology to encourage other countries to use BeiDou.

What to Expect after the Turn?

China’s space industry is likely to become more fragmented in the 2020s, and this is seen as a positive development. To now, almost all space activity in China is in some way connected to CASC, a sprawling company of nearly 200,000 people and business lines in nearly all space-related verticals. This has allowed the Chinese space industry to catch up to the West fairly quickly and consistently, with five year plans, broad industrial development policies, and vertically integrated state-owned enterprises leading the way.

While CASC and subsidiaries will remain the dominant force moving forward in China’s space industry, the private sector will take a bigger piece of the pie. This will be particularly true if CASC were to focus on larger projects such as the Long March-9 super heavy lift rocket, the China Large Modular Space Station, and missions to Mars and beyond. As a greater number of Chinese commercial space companies reach technological maturity, we will likely see these companies move to aggressively address export markets when possible, likely supported by Chinese financing.

Standards will likely be set for activities such as the integration of EO, telecommunications, and navigation satellites, and China will likely attempt to set its own standards for this. Most countries will be unable to support a full suite of space activities, and likely China will open its space infrastructure to other countries in what could be considered an act of goodwill, an attempt to win market share, or both.

Ultimately, while the long-term future of the Chinese space industry remains uncertain, two things seem clear — the trajectory is upward, and 2020 will be a turning point in that trajectory. VS

Blaine Curcio is a Senior Affiliate Consultant at Euroconsult.