Maritime broadband connectivity has been a growth story for the satellite industry in the last decade. This was largely built on the increasing value proposition of Very Small Aperture Terminal (VSAT) solutions. While the introduction of Time Division Multiple Access (TDMA), of other optimization technologies and of the availability of more satellite capacity supported market growth in the early 2010s, it was the deployment of High Throughput Satellite (HTS) systems by several operators including Inmarsat, Intelsat, and others, and of the O3b constellation of SES, that contributed to an expansion of the maritime VSAT market in recent years.

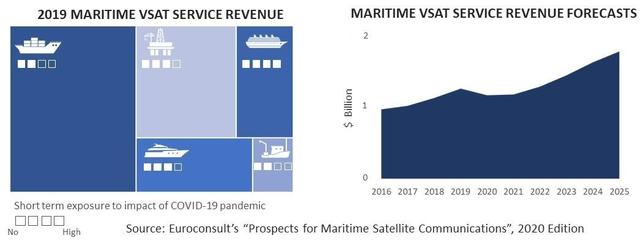

In the latest edition of its annual research on trends and prospects for maritime connectivity, Euroconsult estimated that VSAT service revenues reached close to $1.3 billion in 2019, with an 11% growth over the previous year. Most of the service providers that could be reviewed reported an increase in the number of VSATs installed, for a total of more than 28,000 ships using VSAT connectivity.

Parallel to the overall market growth, several noticeable events took place including the acquisition of Inmarsat by a consortium of private equity funds, the larger entry of SES in the cruise connectivity business, the commercial launch of Iridium’s Certus solution through its Next constellation, among other events.

At the start of 2020, dynamics were still very positive, even if strong competition could impact certain market players. The swift COVID-19 outbreak had a sudden impact on the industry and on the other economic sectors. It is important to understand the large differences between the sub-segments that together compose the maritime connectivity market. We tend to consider five main sub-segments, each of which includes a variety of vessels and organizations. To understand some of the key impacts on the market, let us consider the following: merchant shipping; offshore oil and gas activity; cruise; leisure; and fishing.

Overall, our analysis suggests that data traffic on a ship at sea will not decrease, and could even increase during this crisis period, as both the crew and potential passengers need to collect and exchange information on a very regular basis. The key questions are then how many ships will be in operation, how much ship owners can afford to pay for connectivity, and how exposed are the revenues of service companies and satellite operators in this new environment.

Merchant shipping may be relatively less impacted than certain other subsegments. The need for various goods, and initiatives taken by the International Maritime Organization (IMO) to help maintain operations in various ports, have enabled a continuity in traffic. The considerable slow-down of the economic activity has nevertheless created a large imbalance between supply and demand. The strong drop of the Baltic Dry Index, which measures the cost of shipping goods around the world, to its lowest level in at least five years, certainly suggests a quickly evolving situation and a strong impact on the economics of the shipping business. Some company defaults, a slow-down in new installations, and potentially stronger negotiations on any new service contracts are likely in the coming months.

The cruise and leisure segments have directly suffered from the lockdown currently in place in many countries, including in the U.S. and Europe. Depending on how long the situation lasts, and on the constraints that could apply to their specific operations and on the restrictions for international travel, cruise activity will likely be very low in 2020. When considering connectivity services, the leisure segment tends to work with flexible contracts, as the activity remains very seasonal. As such, connectivity service providers should see a direct impact from a lower yachting activity this year. For cruise ships, contracts might be negotiated for fixed fees or include variable components. Those large clients would furthermore likely be in a position to negotiate amended terms, resulting in a significant revenue exposure for service companies.

In the particular case of offshore operations, the price war that started in the oil market may impact the number of active rigs in the coming months, where the current Brent crude oil pricing currently stands at around $30 after having reached a low at around $20 in April. As was the case a few years back, pressure on the spending and Average Revenue Per User (ARPU) per site could also occur.

Fishing, which remains a relatively small sub-segment, should also be impacted, with operations largely depending on the type of ship and on the area of activity. The impact will likely include a combination of restricted operations and of flexible connectivity plans generating lower revenues for service companies.

Combining all those factors, we anticipate that service revenues for VSAT connectivity could decrease in 2020, for essentially the first time, by up to 7%. These revenues could essentially stabilize and then progressively rebound. The 2020-2021 period should be the most sensitive, with the exposure and dynamics of each service company largely depending on its positioning.

Beyond the immediate impact, the current crisis may have some consequences that could lower the growth potential in the next few years. The first and potentially most important could be delays in the procurement and manufacturing of new ships, as a response to slower economic growth (typically for maritime shipping or even for leisure) and/or to a lower appetite of passengers for cruising. A back-to-normal could take up to several years. Particularly for the year 2021, we anticipate a lower volume of VSAT installations, which should weigh on the revenues of the following year.

A second consequence could be that maritime owners may develop a larger appetite for flexible plans. While their spending would remain stable or could increase over time, this would offer them the possibility to optimize their costs in a low activity period. We anticipate that more contracts could include such clauses, noting that KVH Industries has been a strong promoter of such flexible plans in the last three years.

A third consequence could be a stronger level of competition among service companies, and further potential movements across the value chain. While the process around the Chapter 11 bankruptcy process of Speedcast will be an important element of focus this year, we anticipate that other events could take place. Whether new initiatives involve further consolidation and/or vertical integration, market players will aim at optimizing their value proposition for their clients.

In the long run, the drivers suggesting a need for more capacity and connectivity-related services remain very strong. One of the consequences of the COVID-19 outbreak has been a further acceleration of digital services, either for direct communications or to manage professional services and information on the cloud. In the maritime sector, we anticipate that it should also give a further boost to the willingness of ship owners to take advantage of broadband connectivity onboard the ships for both crew welfare and safety, and for the optimization of their operations. We then anticipate that approximately 50,000 ships should be equipped with VSATs by 2025, with more than a doubling of the volume of leased satellite capacity and service revenues potentially close to $1.8 billion. VS