Since its beginnings, the Chinese space industry has been largely dominated by major state-owned enterprises (SOEs), namely China Aerospace Science and Technology Corporation (CASC) and to a lesser extent, China Aerospace Science and Industry Corporation (CASIC). However, since 2014, the industry has opened to a greater degree of private investment, and in 2018, about 30 companies obtained 3.6 billion yuan ($509 million) in funding, including 1.4 billion yuan ($198 million) invested in commercial launch companies. In 2019, total investment dropped to 1.1 billion yuan ($156 million), of which about half was invested in commercial launch companies. Most recent fund-raising examples include Landspace with 500 million yuan ($71 million) and Galactic Energy with a pre-Series A funding round of 150 million yuan ($21 million). According to data in Euroconsult’s upcoming “China Space Industry Report 2020,” the launch service provider market has attracted more private funding than any other verticals during the past few years, with total funding raised exceeding $710 million.

The Rundown of the Chinese Commercial Launch Industry — A Crowded Field

The Chinese commercial launch industry is, above all, crowded. More than a dozen companies have been established since 2014, and while some are focusing on specific elements of the value chain such as rocket engines, more than half are attempting to develop their own rocket. While some are more well-funded than others, and some more technologically advanced, the industry’s nascency means that there is still significant uncertainty as to which launch companies will survive in the Darwinian world of Chinese tech startups.

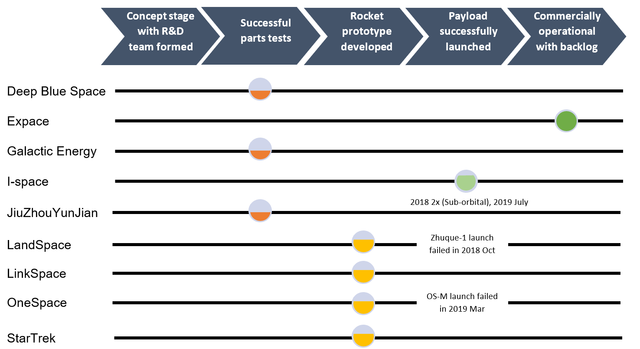

Expace is the most advanced company in terms of technical capability and commercial operation, due in part to significant financial and technological resources provided by CASIC. In 2016, Expace received Series A funding of 100 million yuan ($14 million) and in late 2017 received another 1.2 billion yuan ($170 million), believed to come largely from CASIC. The company’s feature rocket, Kuaizhou-1 (KZ-1), has already completed eight successful launches, including six into the Sun-Synchronous Orbit (SSO) and two into Low-Earth Orbit (LEO). In addition, the company has planned between five and eight launches in 2020. Contracted payloads include Xingyun 01 and 02 for Internet-of-Things (IoT) communications, Changguang for Earth Observation (EO), and WeiliSpace for navigation augmentation. Expace benefits from the best of both worlds — with significant backing from CASIC, the company can count on demand from CASIC-funded satellite initiatives, as well as political support to obtain access to launch sites. In the short-term, however, Expace may face headwinds because it is headquartered in Wuhan, the epicenter of the novel coronavirus outbreak.

Landspace is the most well-funded wholly private launch company in China by some margin — Expace is “nominally private” but better funded. Public sources indicate that Landspace has raised a total of about 1.5 billion yuan ($212 million), and the company CFO noted total funds raised of 2 billion yuan ($283 million) during a conference panel in late 2019. The latest Series C round in 2019 closed at 500 million yuan ($71 million). Noteworthily, the C round was publicly led by Country Garden Venture Capital, the VC fund of the Country Garden Group, a major real-estate conglomerate with a market cap of about 35 billion. Such a large and public endorsement of a space company by such a high-profile VC is unprecedented in China and is indicative that the space industry is attractive to the larger VC world. Euroconsult senior affiliate consultant and China expert Blaine Curcio said: “In 2019 we saw fewer, but larger rounds, as VCs became less risk-hungry towards very early-stage companies, especially in areas such as satellite manufacturing.”

In terms of technical progress, Landspace has completed various phases of engine testing and assembled the ZQ rocket prototype in 2018. Despite the failed attempt to launch ZQ-1 to LEO in October 2018, the company has signed several contracts with customers such as Open Cosmos, D-Orbit, and Spacety. Landspace is actively developing a liquid methane rocket engine, which is the fuel of choice for SpaceX’s Raptor and Blue origin’s BE-4. This is significant for a number of reasons — methane engine design can be less complex and save mass, and methane is significantly easier to store in space compared to liquid oxygen and liquid hydrogen. Also, methane has a higher systematic performance and it can burn cleaner and cooler, making it easier for maintenance and ideal for reusable rockets. Methane offers a lower cost than liquid hydrogen, kerosene, and hydrazine or solid fuel, and it is found on other planets, making it ideal for space exploration.

Beyond Landspace and Expace, i-Space, also known as Interstellar Glory, is targeting to lower the cost of small, eventually medium-sized payloads and providing speedy, flexible service. I-Space is developing both liquid and solid propellant launch vehicles. The company’s Hyperbola-1 will be a four-stage solid launch vehicle, while Hyperbola-3 will be a two-stage liquid carrier rocket. The former will have a takeoff mass of 31 tons, and the latter 95 tons. I-space has conducted two successful sub-orbital launches in 2018 and one successful LEO launch in July 2019. Three cubesats, Satellite Balloon, BP-1B were successfully delivered to the orbit. The company has raised more than 700 million yuan ($99 million) in funds.

OneSpace can be considered the fourth company within the first generation of Chinese launch startups, with the company having raised 800 million yuan ($113 million) after four rounds of funding since its founding in 2015. The company has developed the prototype and successfully conducted multiple suborbital launches. For example, the company launched its OS-X rocket in May 2018 for governmental customer Shenyang Aircraft Design Institute, a subsidiary of the Aviation Industry Corporation of China, followed by a second suborbital launch in September 2018. However, OneSpace failed with its first orbital launch in March 2019. Since then, OneSpace conducted several successful experiments on its Shark 200 engine, however, it has not announced a target date for its next launch attempt. Several of the second generation of Chinese launch startups have been founded by former OneSpace executives, including Space Transportation.

Outside of the first generation of Chinese private launch companies, the most well-funded second-generation company is Galactic Energy, having raised 300 million yuan ($42 million) to date despite having only been founded in 2018. The company aims to develop a reusable liquid oxygen/kerosene rocket. Galactic Energy recently performed a hot fire test for its third stage in December 2019. Galactic Energy plans to fly for the first time in June 2020.

StarTrek focuses on sub-orbital launch vehicles and commercial liquid rocket products. The company successfully launched the rocket to the sub-orbital position in December 2019. The launch did not carry any payload, and was more like a proof of concept. LinkSpace is testing its reusable rocket prototype, RLV-T5. Until now, RLV-TV has accomplished the third hop test with 300 meter flight, powered descent and vertical landing.

Other companies such as JiuZhouYunJian, Deep Blue Space have also made progress in testing launch technologies.

These are the final key takeaways for Chinese private launchers and the potential competitive implications for established launch service providers:

Opportunities

The plethora of commercial Chinese launch companies will, at least initially, primarily serve Chinese demand. By the end of 2018, China had announced over 27 satellite constellation projects including 14 commercial constellation projects. Not all these constellations will launch, and those most likely to launch will likely be spearheaded by CASC or CASIC, and give priority to CASC or CASIC launchers which, in the latter case, would benefit Expace. This being the case, commercial launch companies in China will need to compete for several markets, namely supplemental demand from SOEs, demand from private Chinese constellations, and demand from abroad.

On the SOE side, China’s constellation plans like Hongyan, Hongyun, and Xingyun, involve hundreds or thousands of satellites. The majority of these are likely to be sent into orbit on Long March rockets built by China Academy of Launch Vehicle Technology (CALT) or Shanghai Academy of Spaceflight Technology (SAST), but commercial companies will surely be competing for supplemental launch demand, either based on faster response-time, lower cost, or some other flexibility.

China is home to many commercial constellation plans. Few of these plans are currently well-developed, and even fewer will likely launch in full, but if even a fraction of China’s commercial IoT, EO, and scientific experiment constellations come to fruition, it will represent a large demand foundation for commercial launchers.

Finally, Chinese commercial launch companies will compete abroad. Should the global economy launch further toward a U.S. and China decoupling, we will likely see a large handful of countries like Pakistan, Venezuela, and Russia lean toward the Chinese side of the divide. Even in the unlikely event that the U.S. and China start to see warming relations, it remains likely that commercial Chinese launch companies will compete abroad. This has been seen in recent years with Landspace, Onespace, and others appearing at international conferences such as International Astronautical Congress (IAC), and the Farnborough Air Show.

Challenges

Likely the single greatest challenge facing Chinese commercial launch companies today is the difficulty in securing the initial contracts required to convert a concept from R&D stage to full commercialization. For example, in the United States, NASA and other organizations actively seek out space startups doing interesting things, and they award contracts for projects relevant to NASA programs. This allows the startups to establish a track record, refine their technologies, and pay the bills.

Conversely, in China, the system is rather different. The China National Space Administration (CNSA) acts as the state space administrator, but most contracts are awarded to CASC, with CASC then awarding subcontracts to suppliers. This means that CASC, rather than CNSA, has the ability to choose who gets these sub-contractor contracts. Not necessarily wanting to enable future competitors to grow stronger, CASC is less likely to give contracts to commercial startups. This is even more the case because CASC, a sprawling organization with many capabilities, can likely meet most requirements internally. It is a challenging setup for the upstarts.

Commercial launch companies in China also have funding challenges. While there is a large and vibrant VC community in China, investors tend to have shorter time horizons, typically three to five years, which is challenging for companies in such a nascent industry as rocketry. VC’s apprehension is likely reinforced by regulatory uncertainty and the difficulty of competing with monopolist incumbents.

What’s Next?

Looking forward, the only certainty in the Chinese private launch industry is that the field is likely to thin in the coming years, with the market unlikely to support greater than 10 launch companies. Expace is seen as by far the most likely to succeed, given its relationship with CASIC and the subsequent captive demand that they can expect to enjoy. Landspace and iSpace are positioned as the two next most advanced, followed by OneSpace and Galactic Energy. In the future, more companies will focus on specific parts of the value chain, i.e. manufacturing rocket engines rather than doing the entire rocket. Once Chinese private launchers have built a proven track record from its domestic market, these private firms could potentially become competitors for international companies such as Rocket Lab, SpaceX, and Arianespace.

For a preview of what may be on the way, we can look to the development of China’s state-owned launchers. Thirty years ago, CASC launched its first commercial satellite — AsiaSat-1 — onboard a Long March-3. Two years later, a Long March-2E sent the first international satellite to be launched by China into orbit, Optus-B1, for Optus of Australia. Over the past decade, the Long March family has expanded to more than five variants and has now launched more than 50 satellites for international clients, including Nusat for Argentina, Gomx for Denmark, SaudiSat-5A/B for Saudi Arabia, and others. In January 2020, Argentinian startup Satellogic agreed to send 90 commercial EO satellites into orbit on five to six dedicated Long March flights. While we may still be some years away from seeing similar action from commercial Chinese launch companies, the speed and scale of the market today tell us that it should be a question of when, rather than if that day comes. VS