It’s often said that bad news comes in threes: unfettered price drops, COVID-19, and bankruptcies certainly qualify as events that have shaken the satellite industry to its core. Big, medium, and small players alike have had to find ways to stay afloat in the short term, while preparing for the new normal in the mid- to long term. As the industry digests the news and more importantly, takes steps in managing this triple-whammy impact, players in the value chain are looking for the right market signals, key verticals to target, and recalibrating value propositions that will position their companies for a comeback. The industry’s health is at stake and while there’s no silver bullet — backhaul is one vertical that may prove to be a key market offering to reverse the industry’s fortunes.

As the explosion of data and demand for connectivity grows, the satellite industry has moved from a couple-of-dozens-of-TPEs payloads to Terabytes-per-second satellites, and it is currently making its way to megaconstellations. This is quite a feat for the satellite industry, but it remains a trickle in the overall demand picture given that satcom only captures a single-digit share of total telco traffic. Current and planned supply for capacity in Geostationary Orbit (GEO), Medium-Earth Orbit (MEO), Low-Earth Orbit (LEO) in various frequency bands can and should be easily absorbed as part of the telco toolkit to support data needs. However, can and should are very different things:

● Can satellite capacity be absorbed to support telco traffic? Based on historical telco traffic and predicted growth, satellite capacity can easily be absorbed with broadband access to homes and mobile phones (where most of the traffic is taking place) experiencing network challenges, congestion and lower quality of service, exacerbated during the time of COVID.

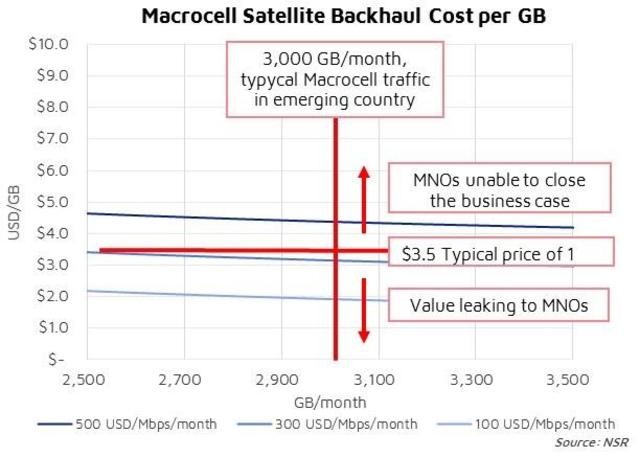

● Should telcos absorb satellite capacity? This is where things get a little bit tricky. Capacity prices, which factor into the Total Cost of Ownership (TCO) equation have prevented telcos from adopting satellite backhaul solutions due to ROI considerations. Simply put, satellite capacity has been expensive, which does not close the business case for telcos in rural areas where satellites are most compelling. The good news is that recently and prior to the onset of the pandemic, satellite capacity price reductions have become critical to unlocking growth in the backhaul market where new price points made ultra-rural network deployments ROI-positive, unleashing solid elasticities and growth.

NSR sees the current average price for large backhaul deployments in the neighborhood of $300 per Mbps/month, which is very much in equilibrium to allow Mobile Network Operators (MNOs) to close the business case and capture a healthy share of the value. It is worth noting, however, that as prices continue to degrade, the industry could see part of the value generation (the average price that the MNO could charge to the end-user) moving to other steps of the value chain, making the margin for the MNO or the integrator greater, but at a loss to the satellite operator.

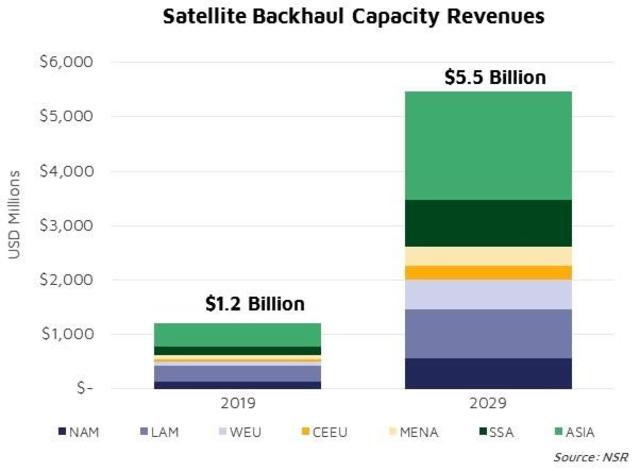

One must also consider that the average price-per-gigabyte the end user is willing to pay also decreases every year, so satellite capacity prices and infrastructure costs should evolve in parallel to keep the business case profitable. On balance, the result from a capacity revenue standpoint, i.e., the business of satellite operators, price drops will actually lead to more than a four-fold increase over a 10-year period as more bits make their way to telco networks.

So in the short term, the industry overall, and satellite operators in particular, are taking a hit due to price pressure. But when we look at backhaul, two of the three bad news items — the COVID-19 pandemic, and continuing price drops — will actually boost demand for connectivity.

Now what about bankruptcies? Intelsat, OneWeb, and Phasor are worth looking into. Intelsat has a large revenue stream and is one of the historical actors in the backhaul and trunking markets. OneWeb represents one of the next-generation programs, with the core mission of bridging the digital divide. Phasor is an antenna manufacturer, which is among a select number of market players poised to enable next-gen programs on LEO constellation platforms.

Bankruptcies are cruel but necessary in order to make the marketplace efficient and in equilibrium. Consider the following:

● It is NSR’s view that Intelsat will emerge from Chapter 11 with C-band compensation to soften the impact, a strong market presence that ensures capturing growth in key segments (mobility, backhaul, etc.) but requiring a healthy balance sheet to invest in the innovations needed to participate in the new market ecosystems like High Throughput Satellites (HTS), service-oriented business models, etc.

● OneWeb may emerge as well or become another entity through an acquisition, partnership, or other arrangement.

● Concerning Phasor, the company had accrued over $300 million in contracts, as well as developed key technologies and relationships throughout the market chain. While generally favorably considered in the flat panel industry, the company was not able to launch product to the market, leading to a make-or-break scenario. However, the company’s R&D developments and value chain support will make their way to the marketplace as well.

There are also key players for next-gen programs that continue to develop their offerings. Cases in point are SpaceX with Starlink and SES’ proposed Non-Geostationary Orbit (NGSO) constellation while Amazon remains at play. Thus, the industry is not stripped of innovation, risk-taking and next-gen, game-changing initiatives.

Overall, bankruptcies lead to a more efficient, competitive, and stronger industry will enhance the value chain and lead the ecosystem to a higher state of balance. Investment funds will be better channeled, value propositions will undergo more rigorous scrutiny, and business cases will need to close. The coronavirus pandemic has hastened the weeding out process, albeit painfully and quickly. But in the new normal or when the recovery ensues, the backhaul market and the industry as whole, will be in a better position to play in the telco/data game.

Bottom Line

In the short term, most projects that were to be rolled out are on hold with the consequent impact on revenues to the backhaul value chain. This impacts all use cases, and the situation will continue until the lockdown is over. Yet, installed sites are seeing a spike in traffic demand. Although it is difficult to monetize this development in the next six to 12 months, mid- to long term prospects given price drops, COVID’s impact to boost connectivity and a more efficient ecosystem will ultimately lead to a stronger backhaul market. The takeaway for backhaul is to ride out the short-term pain in order to cash in on quick, sustainable, and robust long-term gains. VS